Open any news app or social media feed today and you’re likely to come across a variety of stories regarding

However, data from our new Digital 2022 October global statistics report, published in collaboration with Hootsuite and We Are Social, shows that many of these headlines are misrepresenting our digital reality.

So, if you want to understand what the world is really doing online, the good news is that you are in the right place – just read below.

10 best takeaways

If you’re short on time, the YouTube video below will take you through the top 10 stories in this quarter’s data.

However, read below for our full October report and my in-depth analysis of this quarter’s key ideas and trends.

And as this is our final report for 2022, I will conclude this quarter’s analysis with my look at the key themes and trends that I believe will shape and define digital success in 2023.

Before we dive into all of these stories, please read the following notes carefully to make sure you understand how recent changes in the underlying data and research methodologies may impact this quarter’s results.

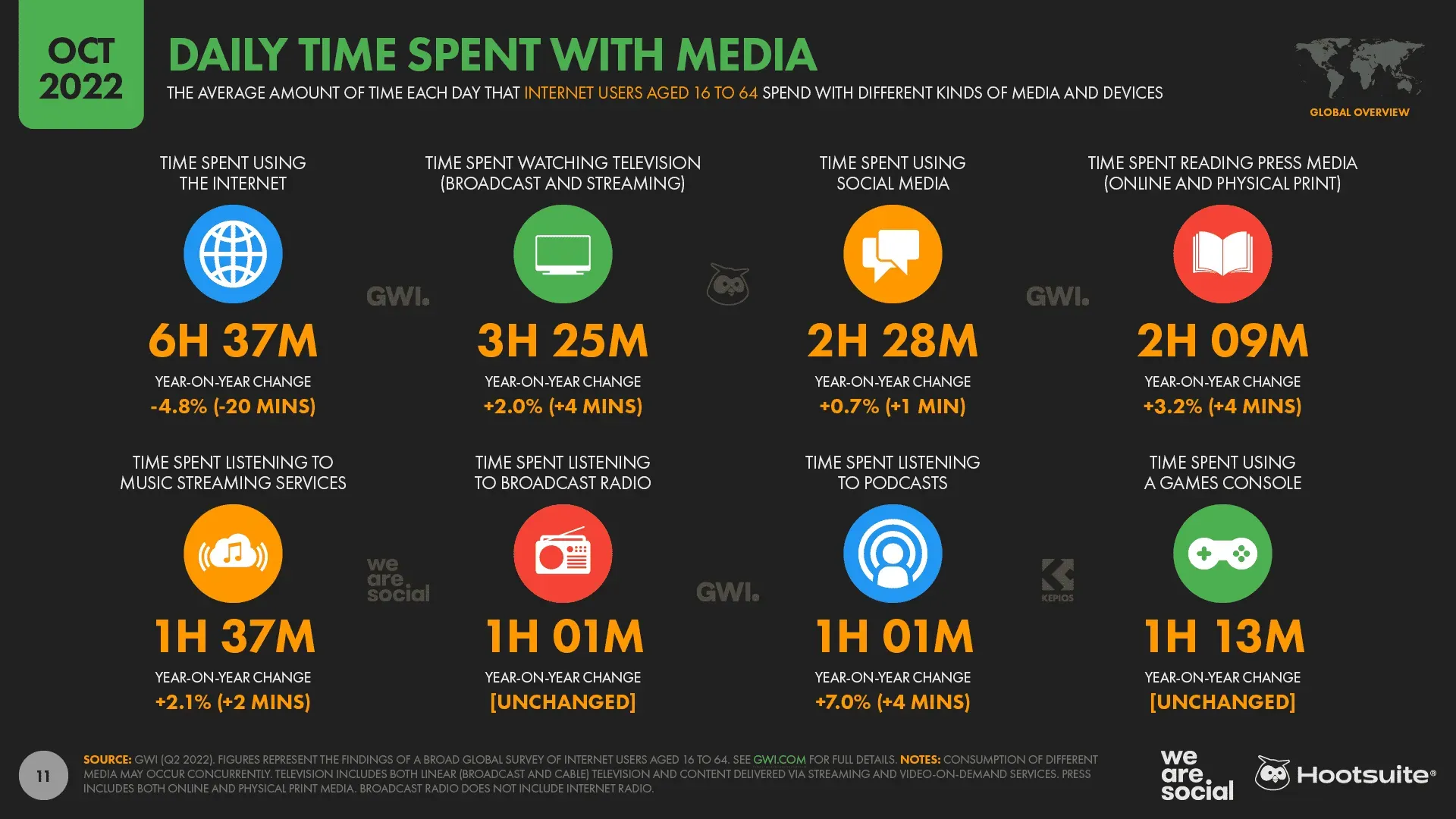

In general, the time we spend online is decreasing, but this does not necessarily mean that the Internet is losing its importance in our lives.

Even with the current average of 397 minutes per day, the typical global internet user still spends over 40% of their lives online.

GWI research and analysis shows that people are trying to become more “purposeful”in their use of the Internet, especially after the rapid increase in time spent on social networks during the quarantine due to COVID-19.

As Tom Morris, Trends Manager at GWI, told us in a recent interview,

“We believe that the world has actually reached a saturation point for time spent online. In recent months, the average daily time spent by users has actually decreased globally, across all generations, and even in growing internet markets such as the Middle East and Latin America. We believe this is mainly the result of a growing distrust of the news and an increase in anxiety caused by social media, especially given that social media accounts for an increasing proportion of total online time.”

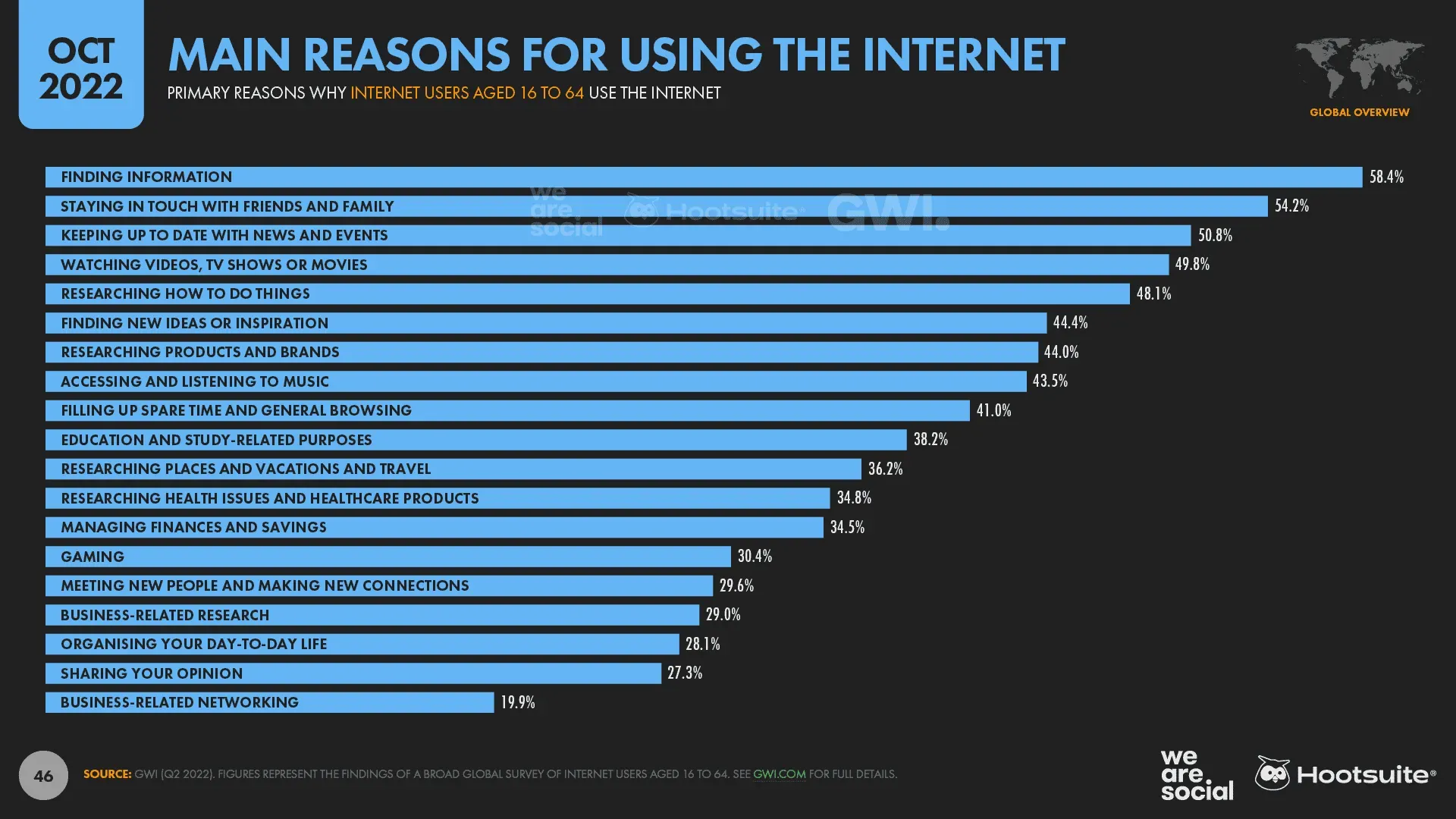

It’s also interesting to note that while people’s motivation to use the internet hasn’t changed much since the pre-COVID era, the number of people who chose each option in the GWI survey has declined across all options.

Again, this change suggests that people can be more “selective”in how they spend their time online, hinting at a more measured and focused approach to using connected technology.

So what does all this mean for marketers?

Well, the key takeaway here is that we also need to be more focused, ensuring that our marketing activities and content actively add value to our audience’s online experience.

In particular, marketers should pay special attention to adding value when they use interrupting advertising formats, especially when it comes to the content we add to social media channels.

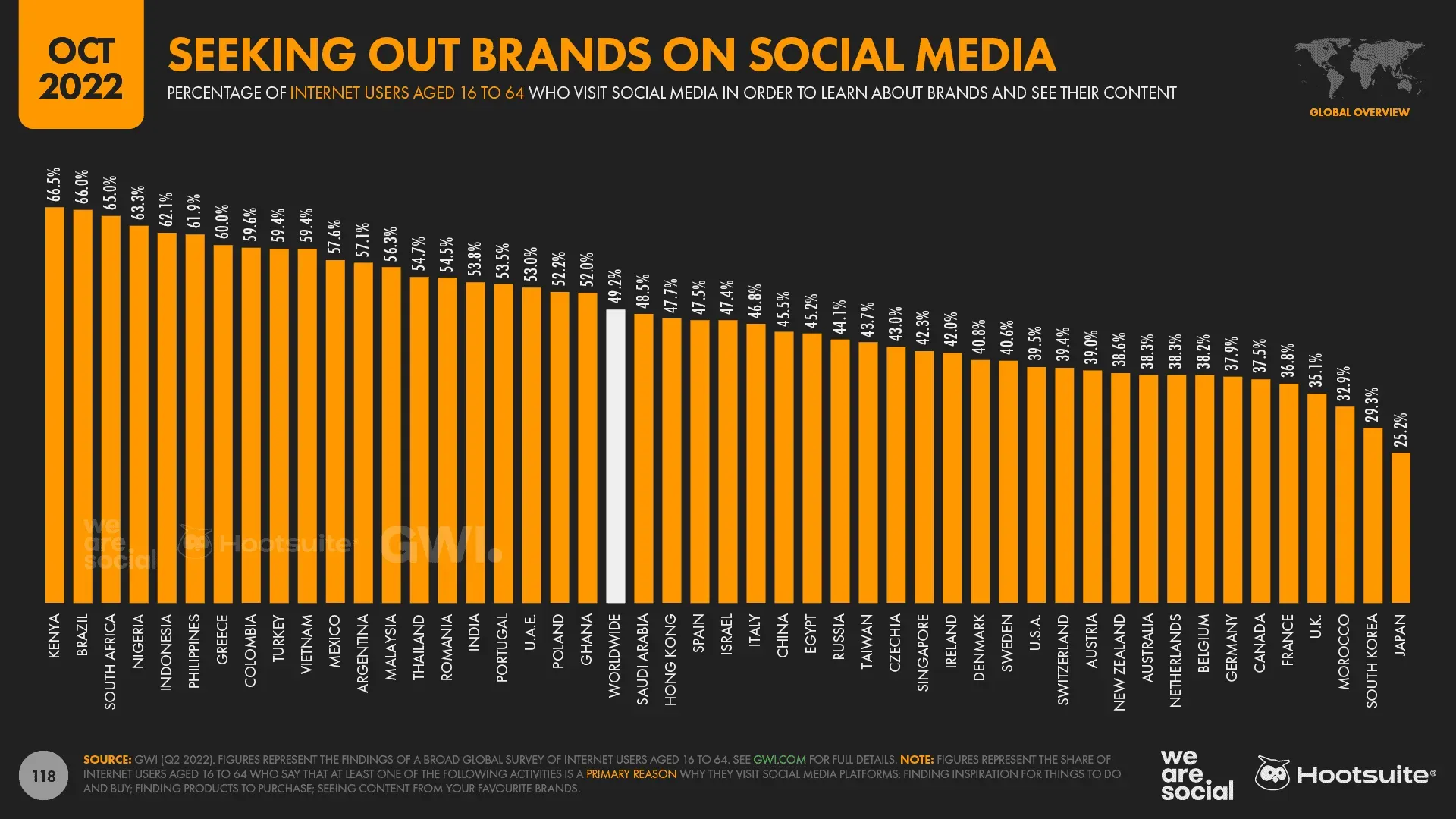

On the one hand, recent data shows that roughly half of all working-age Internet users actively visit social platforms to learn about brands and explore the products and services they are considering buying.

However, as people become more aware of where and how they spend their time online, especially on social media, it’s critical that brands don’t risk annoying their audiences with irrelevant content.

In addition, with many marketers having to cut budgets due to the difficult economic outlook, it is more important than ever for us to ensure that our media and content investments deliver tangible value – both to the audience and to the brand’s bottom line.

Meta Revises Their Numbers… Again

Meta seems to have made even more changes to their ad reach metrics.

The latest numbers posted on the company’s ad planning tools are significantly lower across all three of its ad platforms, even when compared to numbers that appeared on the same tools just 3 months ago:

- Facebook: -4.1% compared to July 2022, corresponding to a drop of 89 million users.

- Instagram: -3.8% compared to July 2022, corresponding to a drop of 54 million users.

- Facebook Messenger: -2.4% compared to July 2022, corresponding to a drop of 24 million users.

- Cumulative reach across all platforms and Audience Network: -5.5% compared to July 2022, representing a drop of 161 million users.

However, such revisions are not uncommon, especially at this time of the year, and we’ve seen the company make similar changes to its reach figures repeatedly over the past decade.

However, we have noticed that such revisions have become more frequent in recent months, and it appears that the company has revised its numbers for Instagram at least twice since the start of 2022.

What’s more, this is the first time we’ve seen the company review metrics for all of its platforms at the same time.

Historically, we have avoided reporting change over time numbers when we discovered these sorts of fixes because a subsequent change in published numbers does not necessarily correlate with an actual drop in “genuine”coverage.

For example, these changes may reflect the removal of duplicate and “fake”accounts, and therefore a decrease in registered reach does not necessarily mean that marketers can reach fewer “real”people in their target audience.

However, given the magnitude and frequency of recent changes, we’ve decided to publish this change data to help marketers make more informed decisions.

This is partly because Facebook’s potential global ad reach figure published in the company’s tools is now lower than the figure the same tools reported this time around four years ago.

In October 2018, Meta scheduling tools reported a potential global Facebook ad reach of 2.091 billion, but today the figure is only 2.079 billion.

Facebook Perspectives

However, it is unlikely that recent changes in ad reach as reported by Meta will correlate with an equivalent drop in monthly active users (MAU).

The company announced a decline in monthly active users in its second-quarter earnings report, and Zuck and his team may well announce a similar trend in the company’s next report to investors.

But Facebook’s MAU decline between April and June 2022 was only 2 million users, which equates to a drop of just 0.1% of the global average — significantly less than the 4.1% drop in ad reach over the same period.

Based on the size of this difference, I believe changes in reporting methodology are likely to be the main contributing factor to Meta’s recent drop in reported ad reach rather than the sudden drop in active users.

The company’s ad planning tool guide reinforces this hypothesis, with a pop-up note next to the reported ad reach figures now saying that this metric is “in development”:

“A metric in development is a measurement that we are still testing. We’re still developing the best way to measure something, and we can make adjustments until we get the right result.”

The note goes on to explain why existing metrics, such as ad reach, can be reclassified as “in development”:

“We frequently launch new features and new ways to measure the effectiveness of those features. Sometimes we publish these metrics, even if the way they are calculated is not final, to get more feedback, improve them, and determine the best way to measure performance.”

However, whatever the reason, the latest numbers are still well below the potential reach that Meta Tools reported just a few months ago.

As a result, marketers must carefully study the latest ad reach metrics for their brands’ specific audiences in order to understand and quantify what paid media activity might be garnered.

It is also important to highlight that the potential ad reach figures published in the Meta planning tools are highly dependent on the number of people who were shown ads on various platforms in the previous 30 days.

As a result, keep in mind that any reduction in reported potential reach may also depend on the number of advertisers buying ads on the Meta platforms, as well as the extent of their media spending.

For example, reducing the number of advertisers, or the amount those advertisers spend on each platform, could result in fewer users seeing ads on the Meta platforms, which in turn could affect the potential reach metrics reported by the company’s tools.

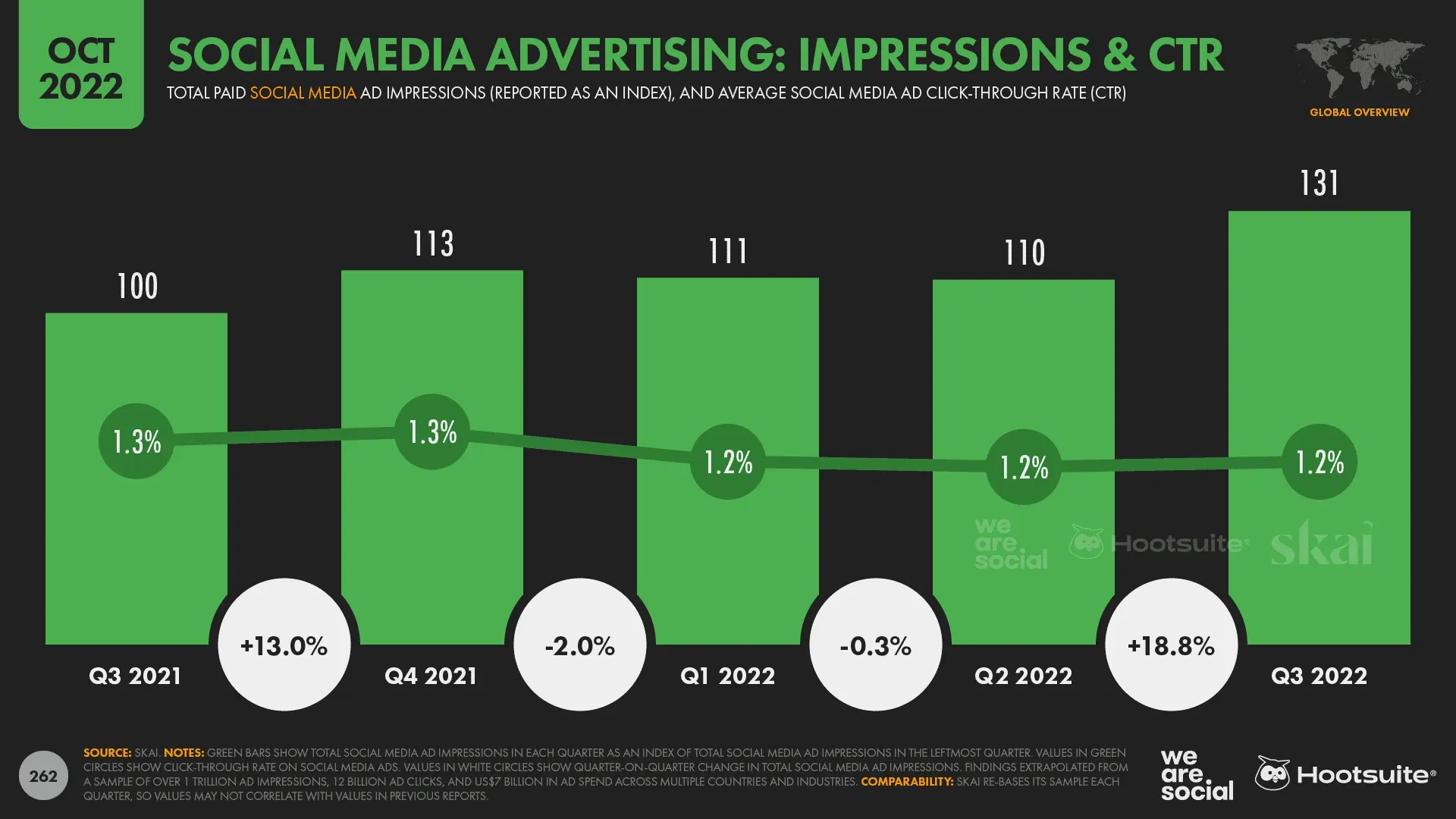

However, Skai’s latest data shows that marketers actually spent more on social media advertising in the third quarter of 2022 compared to the second quarter.

What’s more, the average social media CPM (the cost of displaying 1,000 social media as impressions) has actually decreased in the last 3 months, so the increase in investment resulted in an 18.8% increase in the number of social media ads that were shown to users during all social networks. platforms.

As a result, if the number of advertisers and the size of their investments were to affect the decline in registered reach across Meta’s various platforms, this could indicate a decline in Meta’s share of the overall social media advertising market.

Facebook is not dying

Spoiler: no.

Investors and marketers will want to keep a close eye on how these numbers develop, but it’s important to stress that Facebook is still far from dead.

To be clear, media hyperbole related to Facebook’s supposed “imminent demise”is nothing new, and a New York Times headline condemned “Facebook Exodus”back in August 2009.

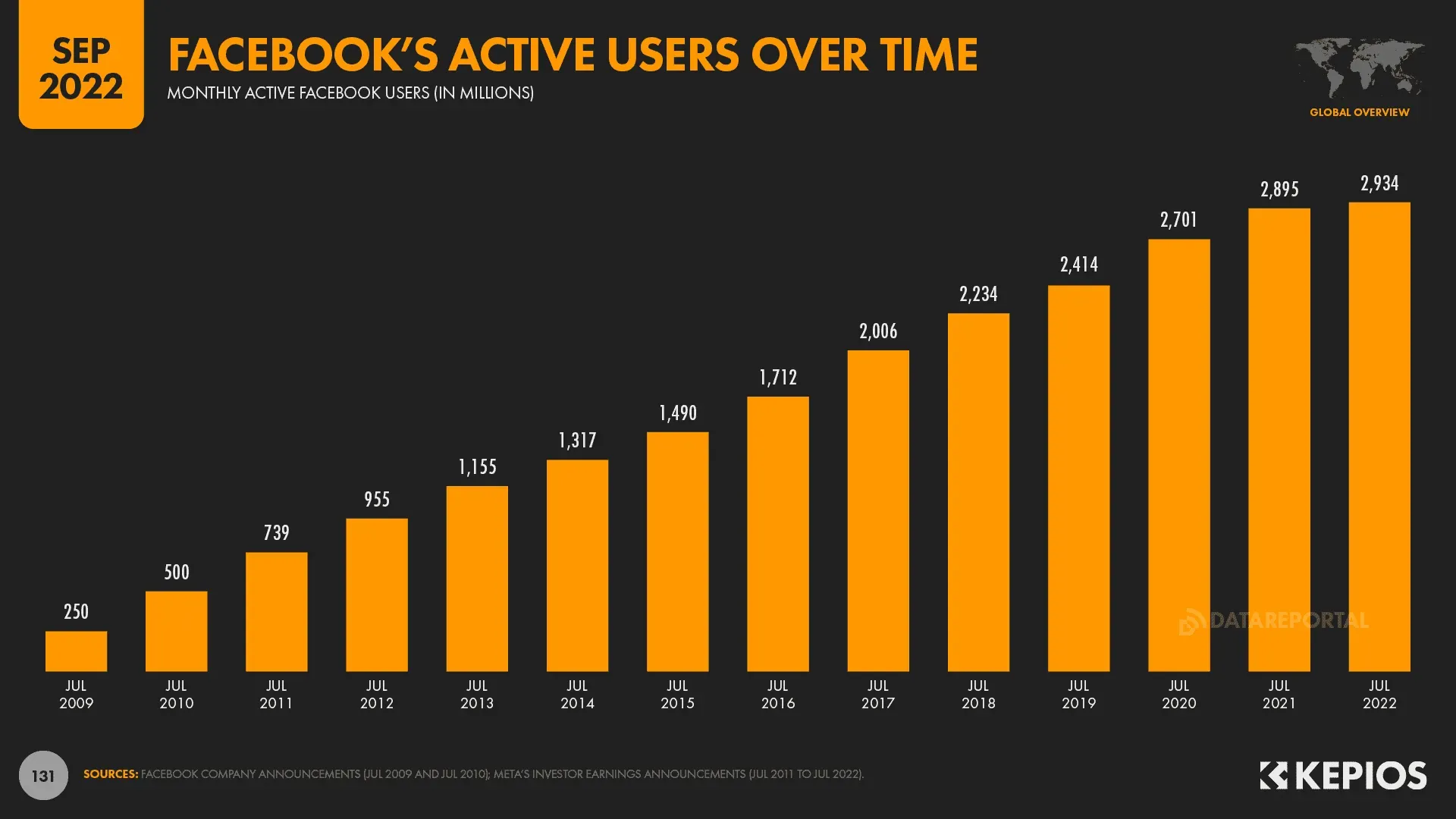

Since then – even after the recent drop in global MAUs – Facebook’s active user base has grown more than 10 times.

However, despite these impressive growth numbers, hardly a week goes by without another clickbait headline with dubious data readings.

Of course, there are a lot of things keeping the Mountain View crew up at night, from reduced usage among teenagers in its most valuable market, to current regulatory issues.

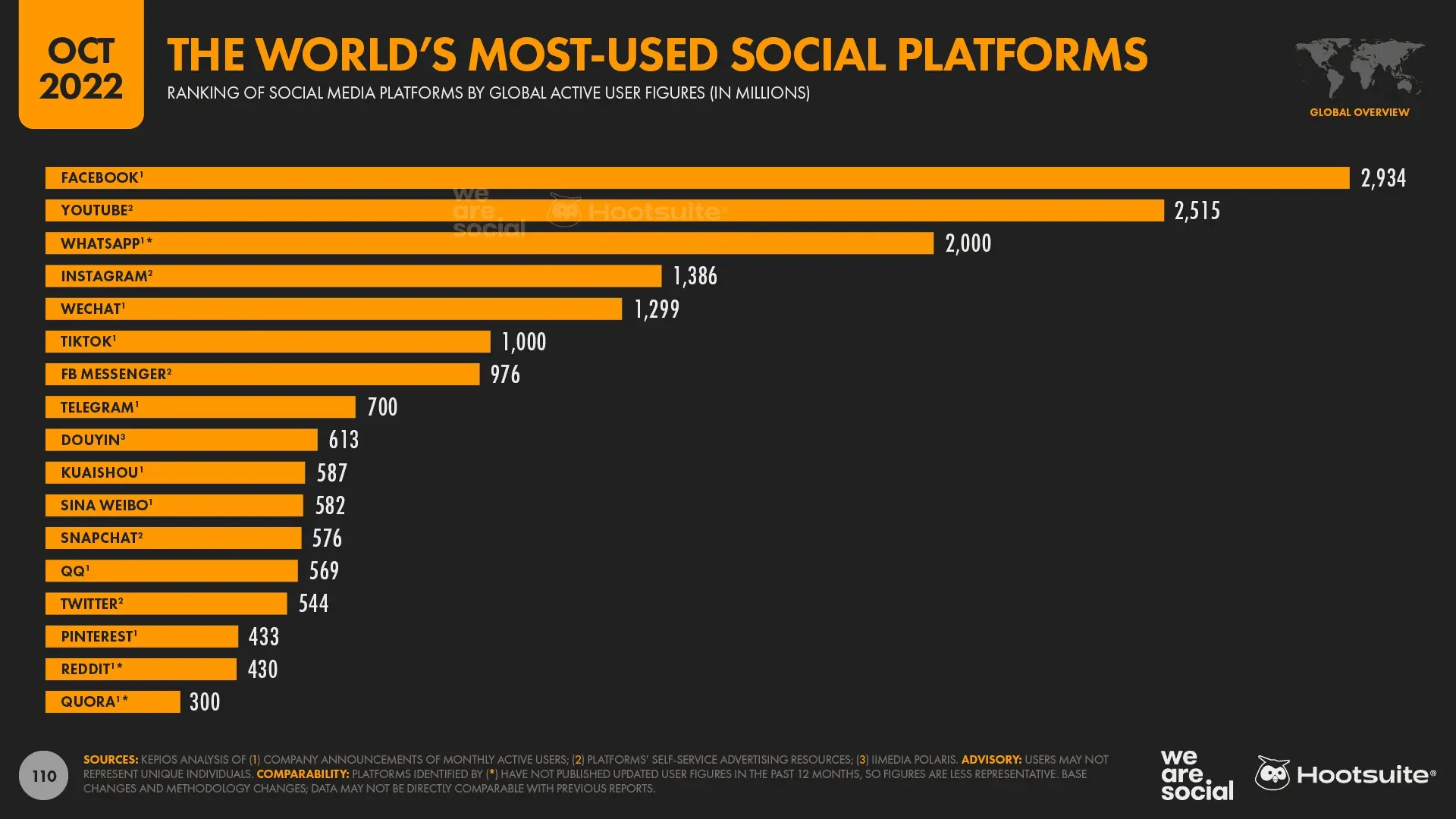

However, Facebook is still the most used social platform in the world and the available data suggests that it still has hundreds of millions more active users than its closest competitor.

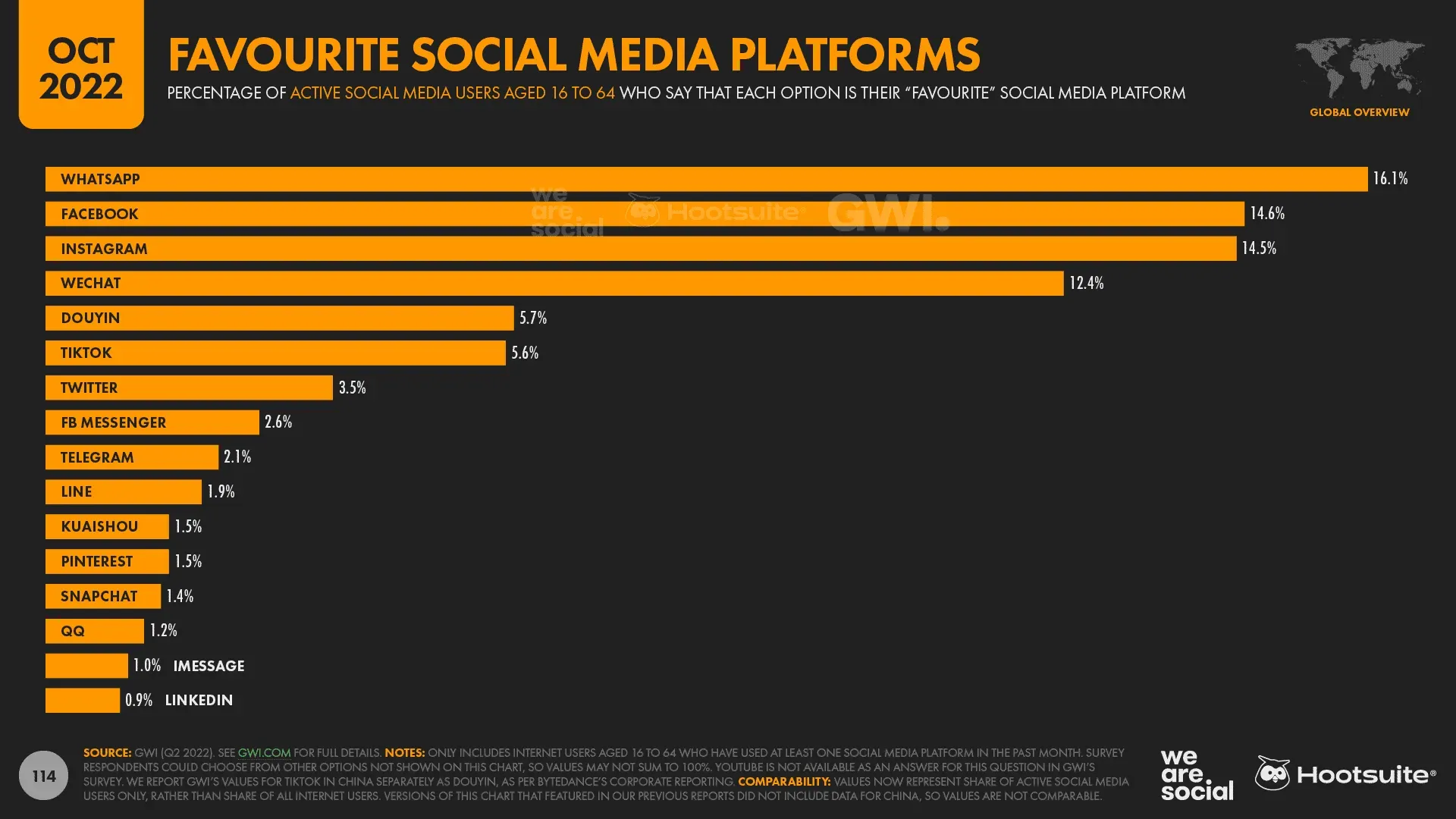

Meanwhile, Meta still accounts for all three of the world’s “favorite”social media platforms, and most importantly, people are still two and a half times more likely to choose Facebook as their favorite social platform than TikTok.

Moreover, analysis of data.ai shows that the amount of time a typical user spends using the Facebook app has actually increased in recent months, from an average of 19.4 hours per month in the first quarter of 2022 to an average of 19.7 hours in month. in the second quarter.

But what about the future?

Well, even if Meta announces a further decline in the number of active users in the coming months, it will likely be many years – and possibly even decades – before Facebook actually “dies.”

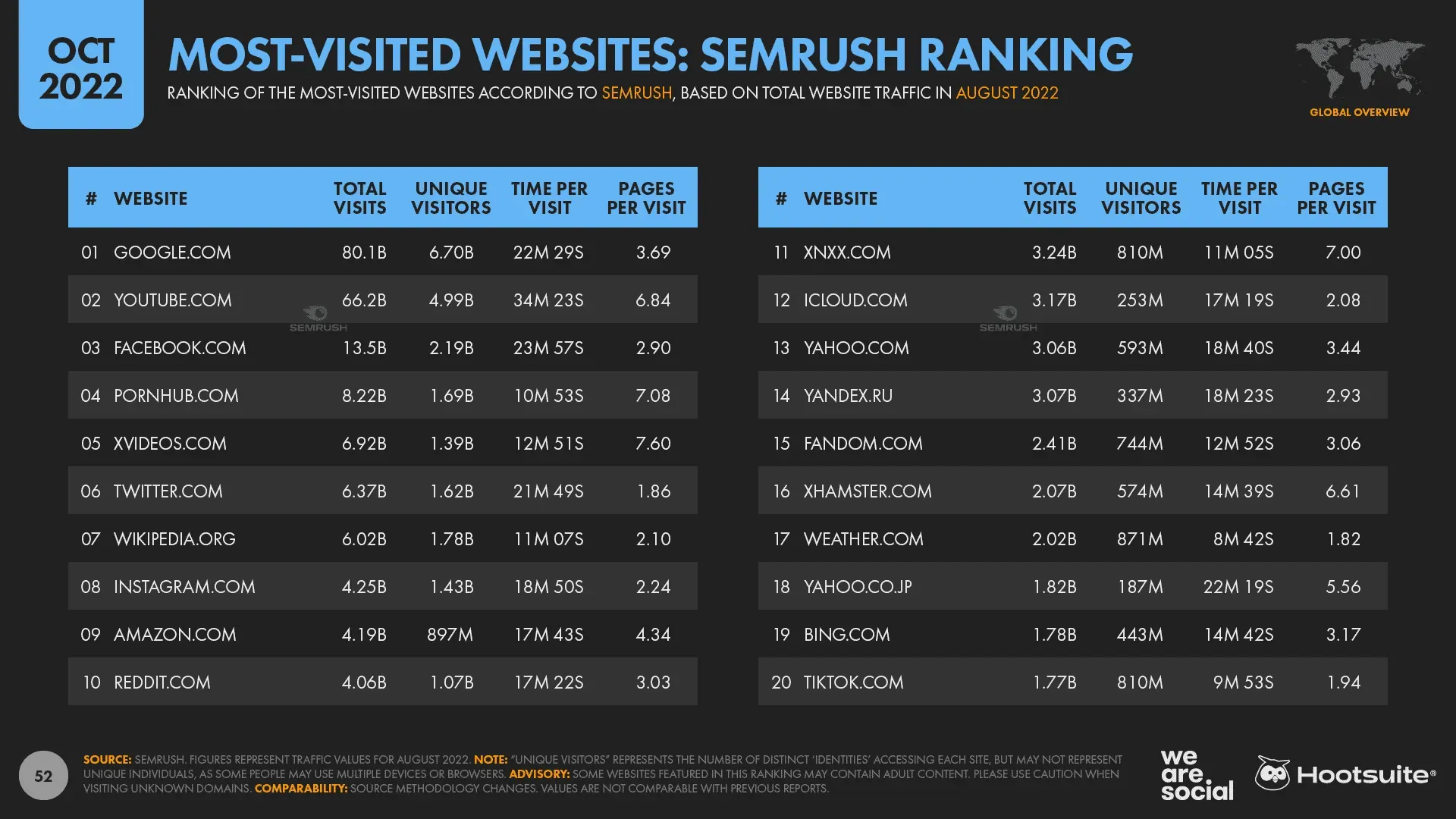

For context, Semrush data reports that over half a billion people still visit Yahoo! every month, despite the fact that the platform has all but disappeared from the media headlines in recent years.

Based on these Yahoo! trends, we can expect Facebook to continue to reach billions of people for the foreseeable future.

As a result, you can be sure that Facebook will continue to offer valuable marketing opportunities far beyond even your most ambitious media plan.

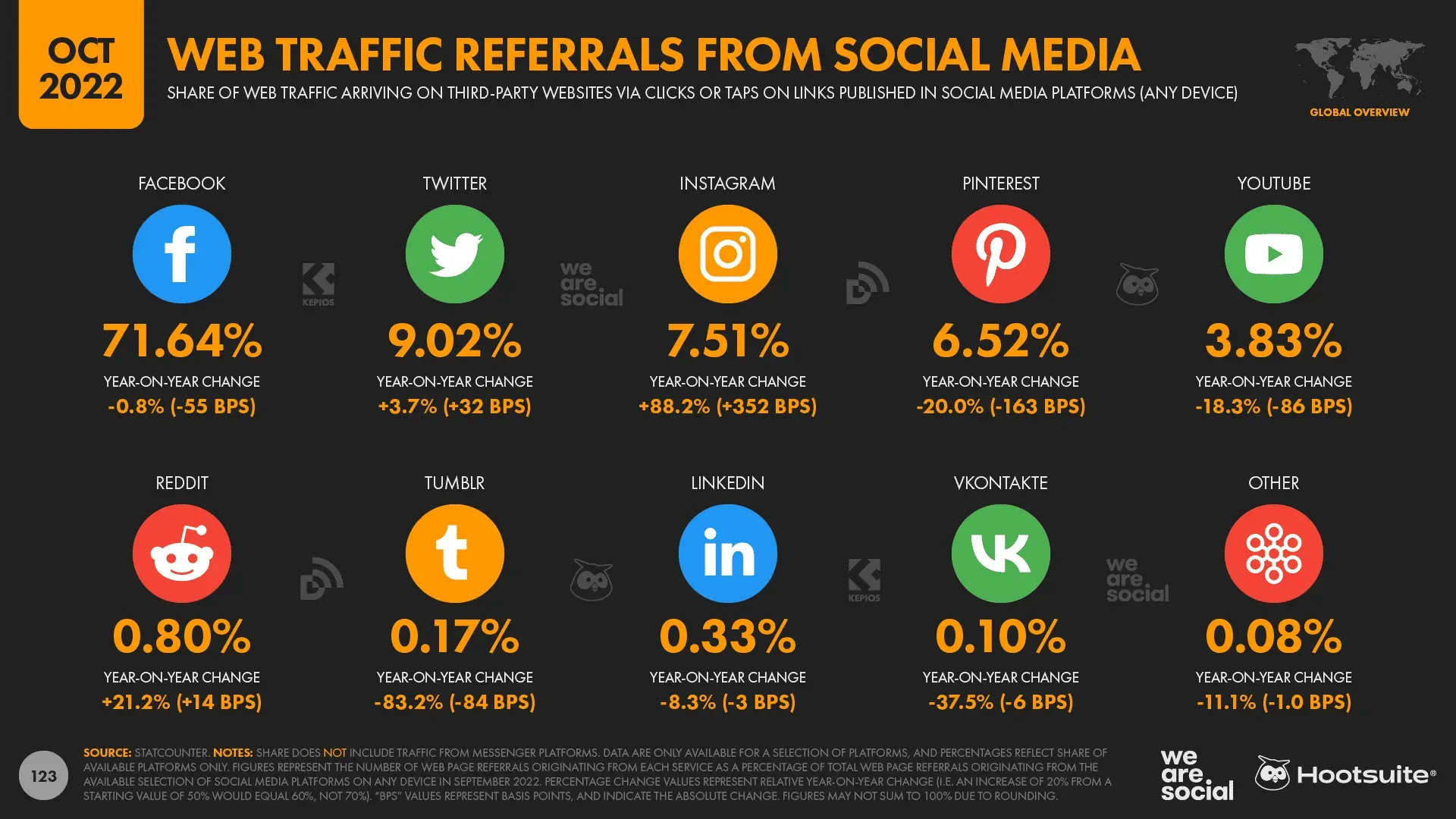

And if you’re still unsure, take a look at this latest data from Statcounter, which shows that Facebook is still responsible for over 70% of all social media web traffic.

How Facebook is different from TikTok

But while we’re on the subject of how headlines can distort our point of view, let’s compare Facebook’s latest numbers with some of the other platforms that seem to be modern media darlings.

To be clear, I am not defending Facebook here; I just want to provide some objective perspective.

First, the numbers reported in each company’s ad scheduling tools show that marketers can still reach twice as many adults aged 18 and over with Facebook ads as they can with TikTok ads.

Of course, the numbers for teens might look a little different, but Bytedance’s tools don’t report data for users under 18, so it’s hard to say for sure.

What’s more, if you’re not actively targeting teens, trends among younger users offer little more than nothing, and – as a marketer – you better focus on what your specific audience is actually doing today.

Next is BeReal.

Yes, the platform is causing a lot of buzz, and yes, the platform seems to be growing rapidly.

Indeed, Sensor Tower data shows that since its launch just 2 years ago, the app has been installed on a total of 53 million smartphones.

However, it is important to emphasize that this figure does not correspond to active users, and August 2022 data shows that the application currently sees only 10 million daily active users.

And even if that number were to double since August, Facebook’s active user count would still be about 100 times that of BeReal.

None of this means that BeReal and TikTok are certainly bad choices; I’m also not saying that you should definitely prioritize Facebook.

I just wanted to add some realism to your plans for 2023.

As a reminder, our job as marketers is to build brands and drive sales, not to jump on all the latest fashion trends.

Of course, if you see a clear way to achieve efficient and effective results with the hottest new platform, by all means go for it.

But don’t expect magic from a platform just because it hits the headlines.

Critically, if you haven’t done the “magic”on Instagram or TikTok yet, there’s no reason to expect you’ll do better on BeReal or the next popular platform that’s sure to follow.

And that’s because the users of any particular social platform are basically the same, even if each platform offers a slightly different demographic profile and slightly different opportunities to engage people.

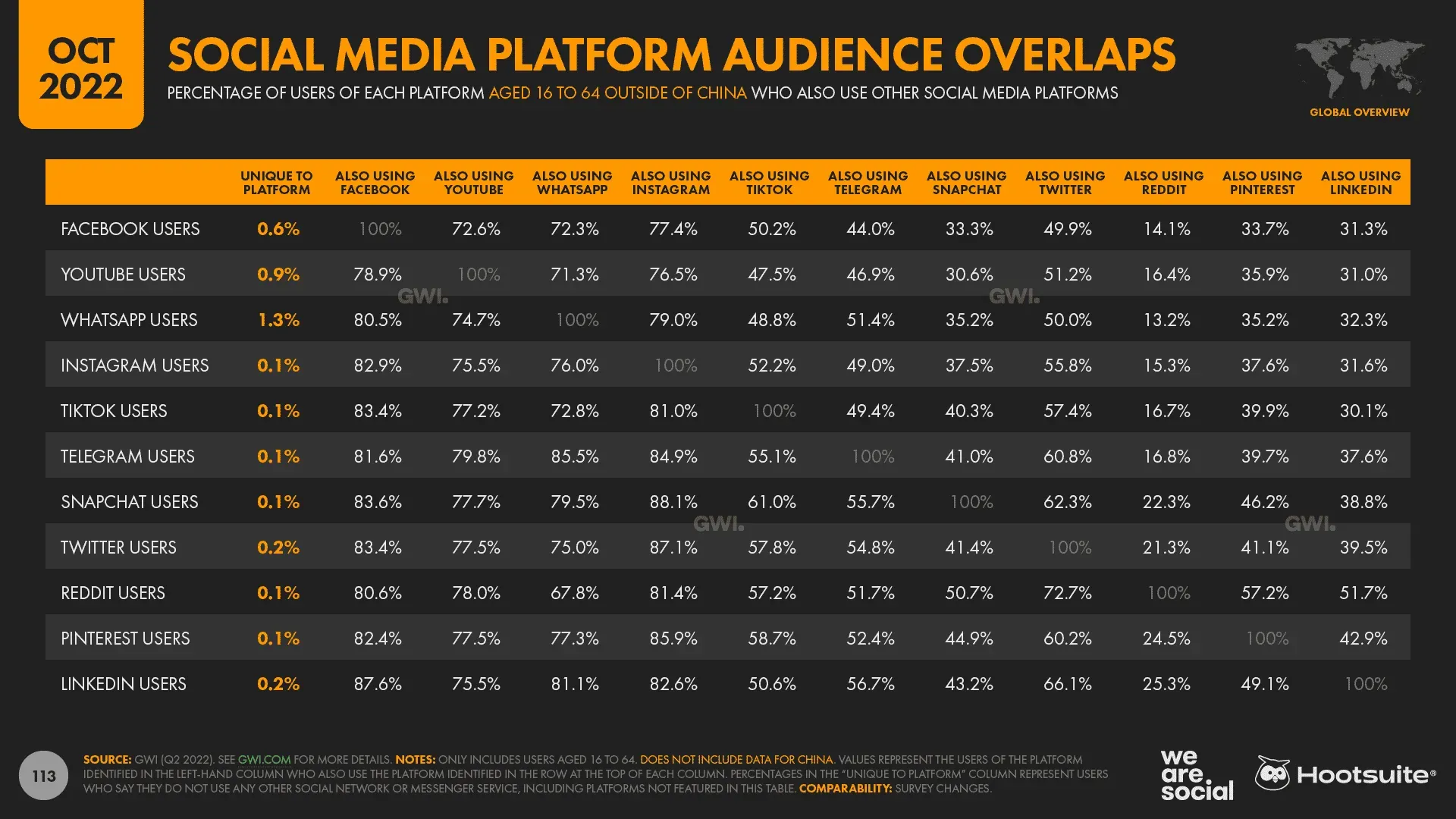

For context: 95% of working-age internet users say they use messaging apps and social media every month, so it’s unlikely you’ll be able to connect with any “unique”users on a new social platform.

Indeed, as the excellent GWI data in the chart below shows, even the largest and most established platforms can barely claim 1% unique reach, while less than 1 in every thousand users on newer platforms like TikTok can be considered unique..

So, given that marketers around the world will be under scrutiny in the coming months as fiscal belts tighten, my advice would be to stick with tried and true favorites like Facebook in favor of “brilliant new properties.”

The Metaverse hype hasn’t paid off (yet)

But the impact of clickbait is not limited to social media.

Another headline that’s been going around in circles in recent weeks concerns the growth of the Metaverse – or rather, the alleged lack of growth.

A widely circulated article published by CoinDesk reports that Decentraland’s virtual world has only 38 active users despite having a market value in excess of US$1 billion.

And no, this is not a typo – the active user number indicated was really only 38.

However, later in the same article, it is acknowledged that this figure, obtained by CoinDesk from DappRadar, is only the number of “unique wallet addresses” that have interacted with the Decentraland smart contract.

In other words, this figure only includes those users who have made an active purchase in the Decentraland environment and completely ignores everyone who has logged in without making a purchase.

However, this is clearly a very “selective”use of data, especially as such a narrow definition overlooks various popular activities such as virtual concerts and fashion shows.

For example, Nielsen (via Statista) reports that over 12 million users attended Travis Scott’s 2020 Fortnite astronomy event.

So it’s perhaps unsurprising that Decentraland has been pretty blunt about CoinDesk’s claims, calling the user metrics cited in the article “inaccurate.”

However, in a response posted on its own blog, Decantraland also revealed that it currently has less than 57,000 monthly active users.

That’s certainly a lot more than 38, but – with a reported valuation of over a billion dollars – each MAU would cost over $17,500 each.

Of course, investors likely expect the number of active users to increase over time, but the same blog post also shows that Decantraland’s monthly active users have actually declined after the “early metaverse hype at the end of 2021.”

So, are the skeptics right – is the “Metaverse”really just empty talk?

Well, other data suggests otherwise.

Of course, user data for Decentraland and Sandbox isn’t very enthusiastic (yet), but similar data for other “virtual worlds”looks much more promising.

Part of it comes down to definitions, of course, and each person’s point of view may vary depending on how they think about the Metaverse.

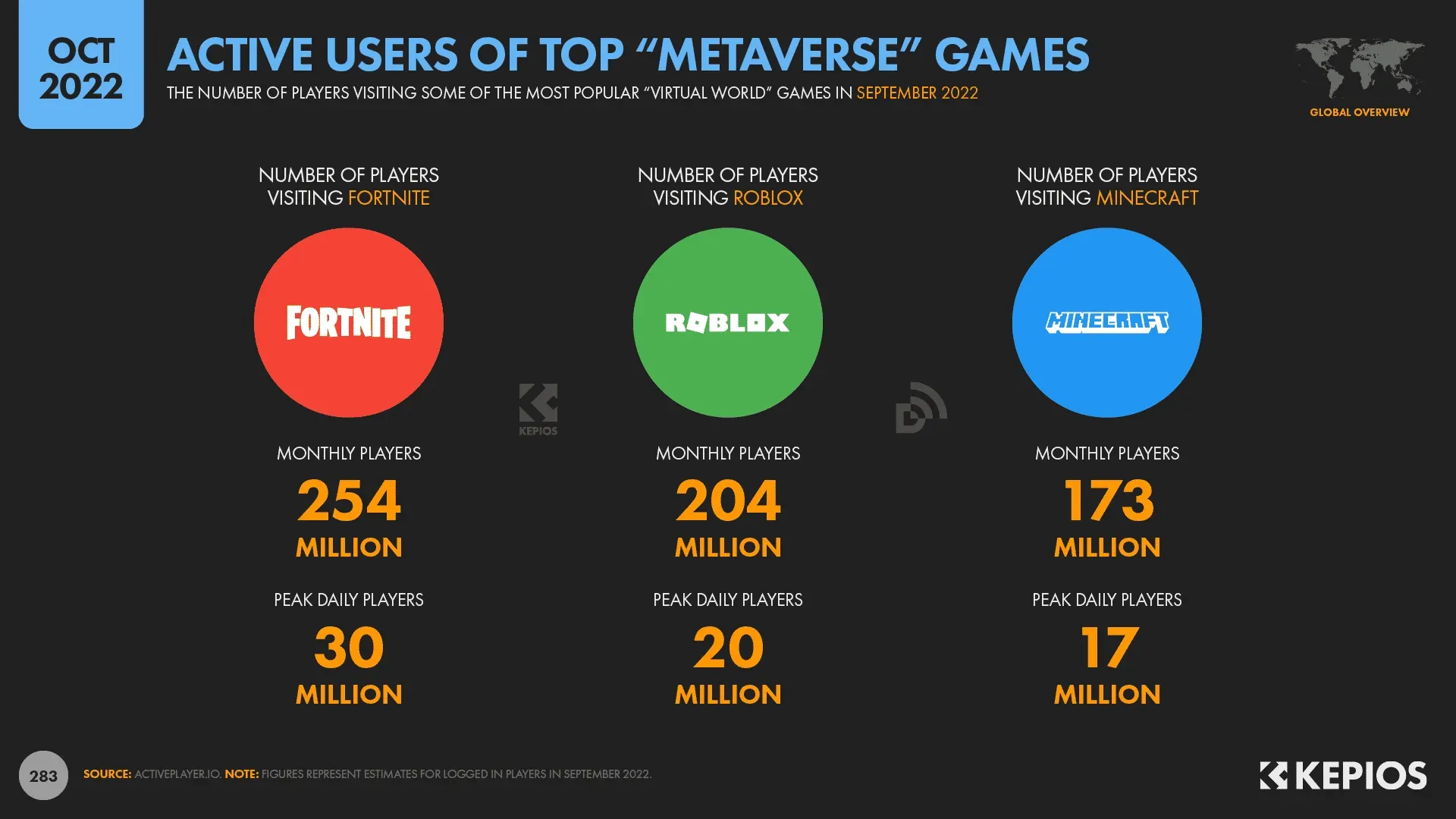

For example, if you want to include immersive games that feature real-life experiences in your definition of the Metaverse, there are already a lot of impressive numbers to explore.

First, ActivePlayer.io’s analysis shows that Fortnite, Roblox, and Minecraft – all of which can be qualified as “virtual worlds”like the Metaverse – are already attracting hundreds of millions of monthly active users (MAUs):

- Fortnite: 254 million monthly active users in September 2022, peaking at 30 million daily.

- Roblox: 204 million MAUs in September 2022, with a peak of 20 million per day.

- Minecraft: 173 million monthly active users in September 2022, peaked at 17 million daily.

So, despite the sensational headlines that offer a very selective reading of the data – albeit in both directions – there is also plenty of real evidence that the Metaverse does indeed have potential.

However, it remains to be seen if this potential goes beyond the current gaming focus and exactly how much this potential is worth.

As a result, Metaverse’s marketing opportunities are still limited to brands that sell items like NFTs in virtual worlds, or brands that can turn their virtual world exploits into real PR.

So, while we will certainly continue to track the popularity of virtual worlds, if you don’t already see an obvious way to tap into these environments, I would suggest you spend your marketing dollars on something else – at least for the time being. existence.

So, back to the “real”world…

YouTube ranks first in time

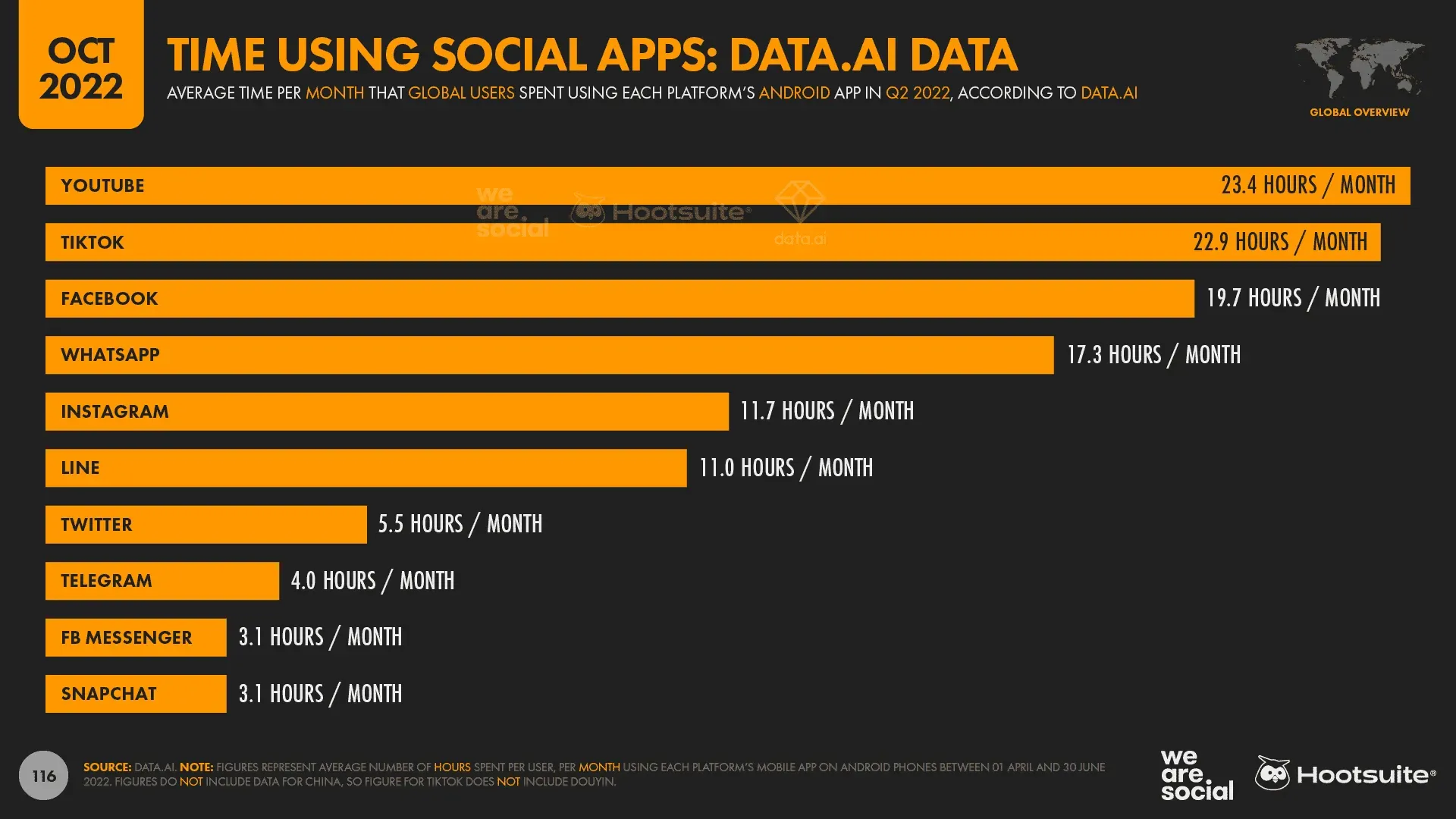

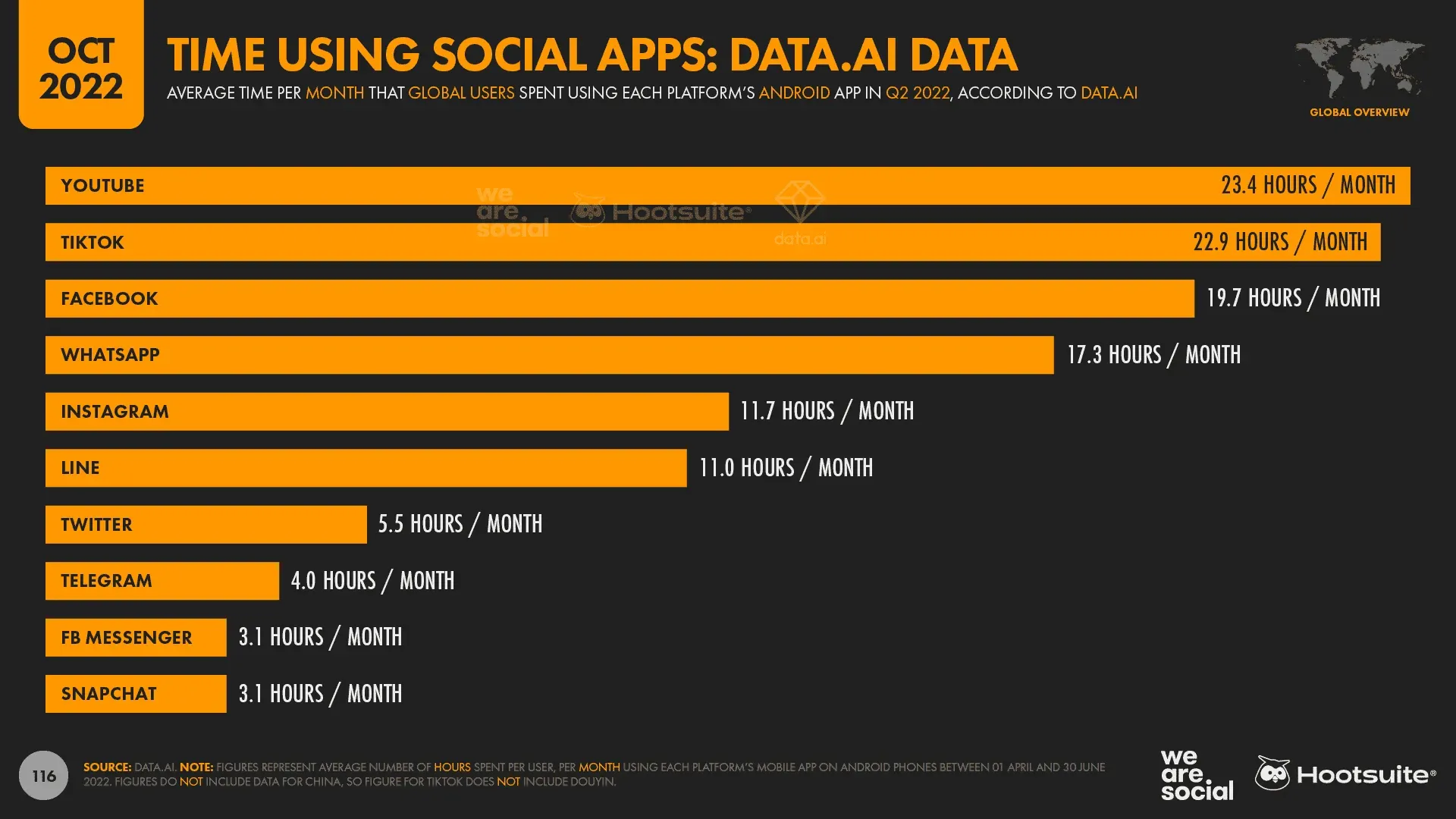

As you may have noticed in one of the charts we’ve provided above, YouTube has reclaimed the top spot in data.ai’s latest social media app rankings for average time spent on them.

The typical user spent an average of 23.4 hours each month using the YouTube app between April 1 and June 30, 2022, which equates to almost a day and a half of total waking time.

TikTok returned to second place in the Q2 rankings, with users outside of mainland China spending an average of 22.9 hours per month on the short video platform in Q2 2022.

However, as we noted above, data.ai’s numbers are better for Facebook, with average monthly time per user increasing to 19.7 hours per month in Q2, up from 19.4 hours per month in the first three months of 2022.

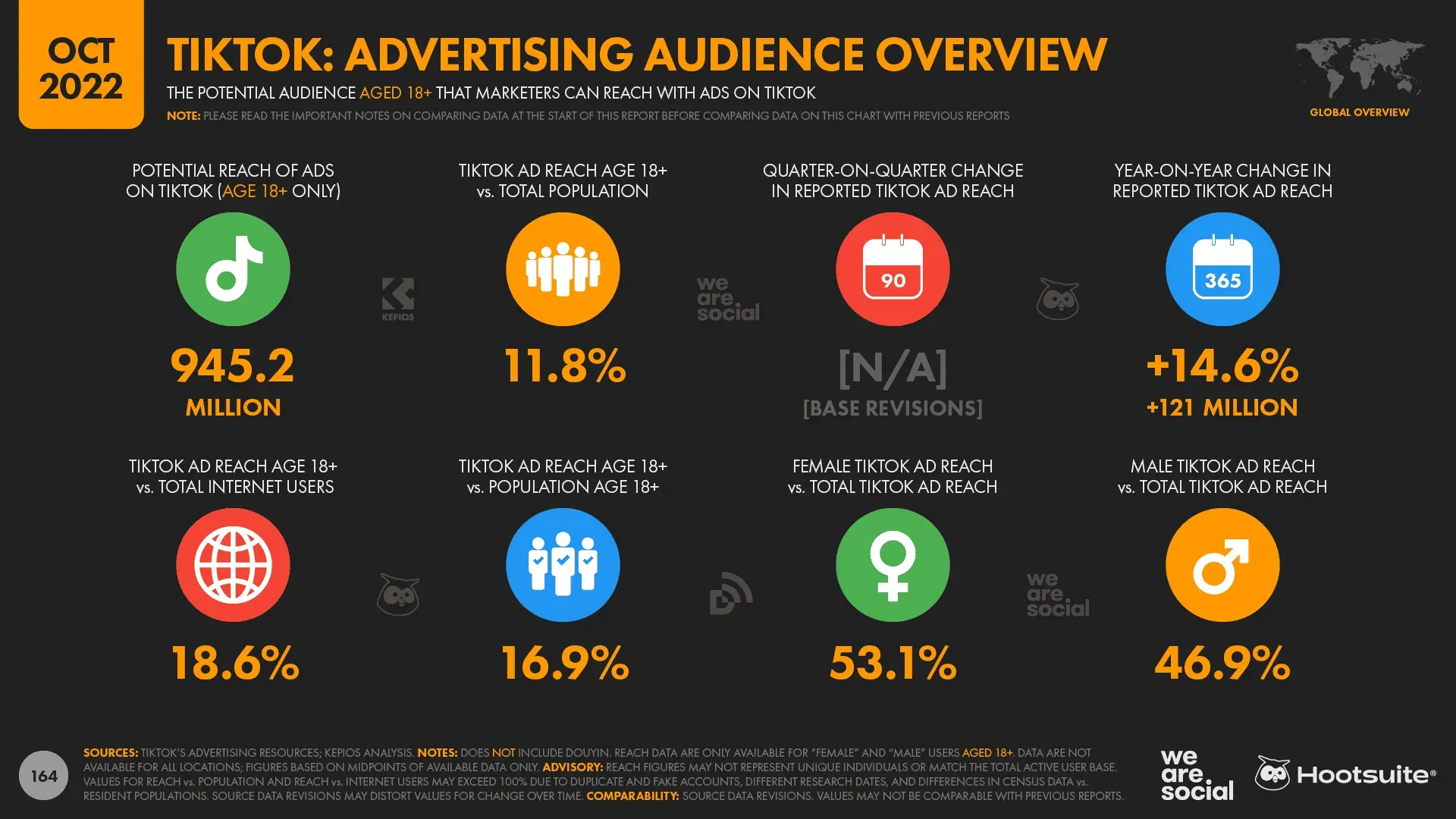

TikTok continues to grow

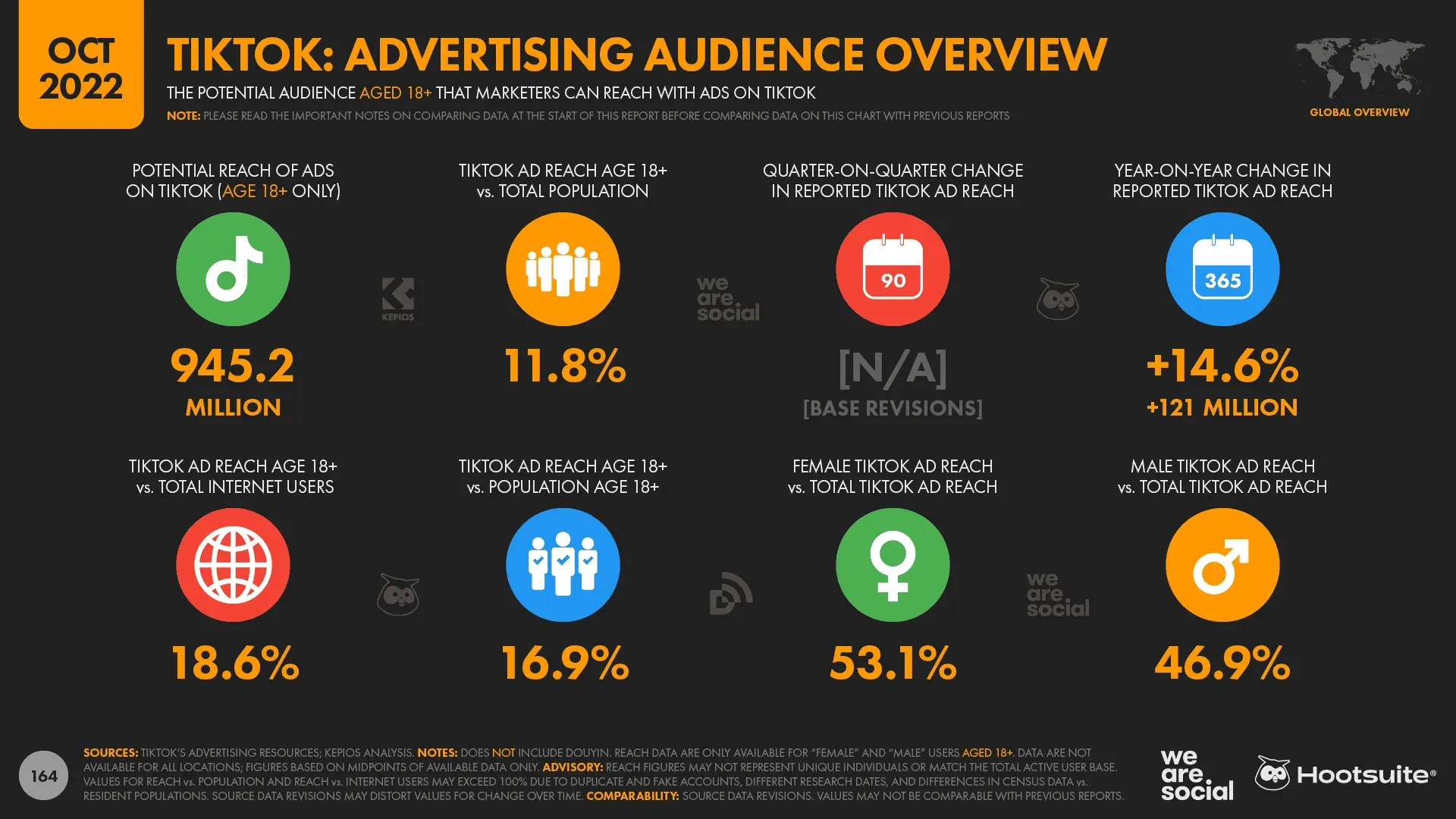

Due to the nature of how Bytedance’s tools report potential ad reach across different services, we have revised TikTok’s ad reach metrics in our October 2022 report.

However, it is important to emphasize that these numbers do not represent a decline in TikTok usage compared to previous quarters.

Rather, the difference in our reported numbers is the result of a change in the input we use to calculate the numbers we report.

Based on these changes, our latest analysis shows that TikTok ads now reach 945 million adults over 18 every month, up 121 million from just 12 months ago.

TikTok’s ad reach has grown by 14.6% over the past year, and now the platform’s ads reach more than 1 in 6 adults on Earth every month.

TikTok revenue continues to rise

And it’s not just TikTok’s ad reach that’s growing; users keep spending more and more money on the platform.

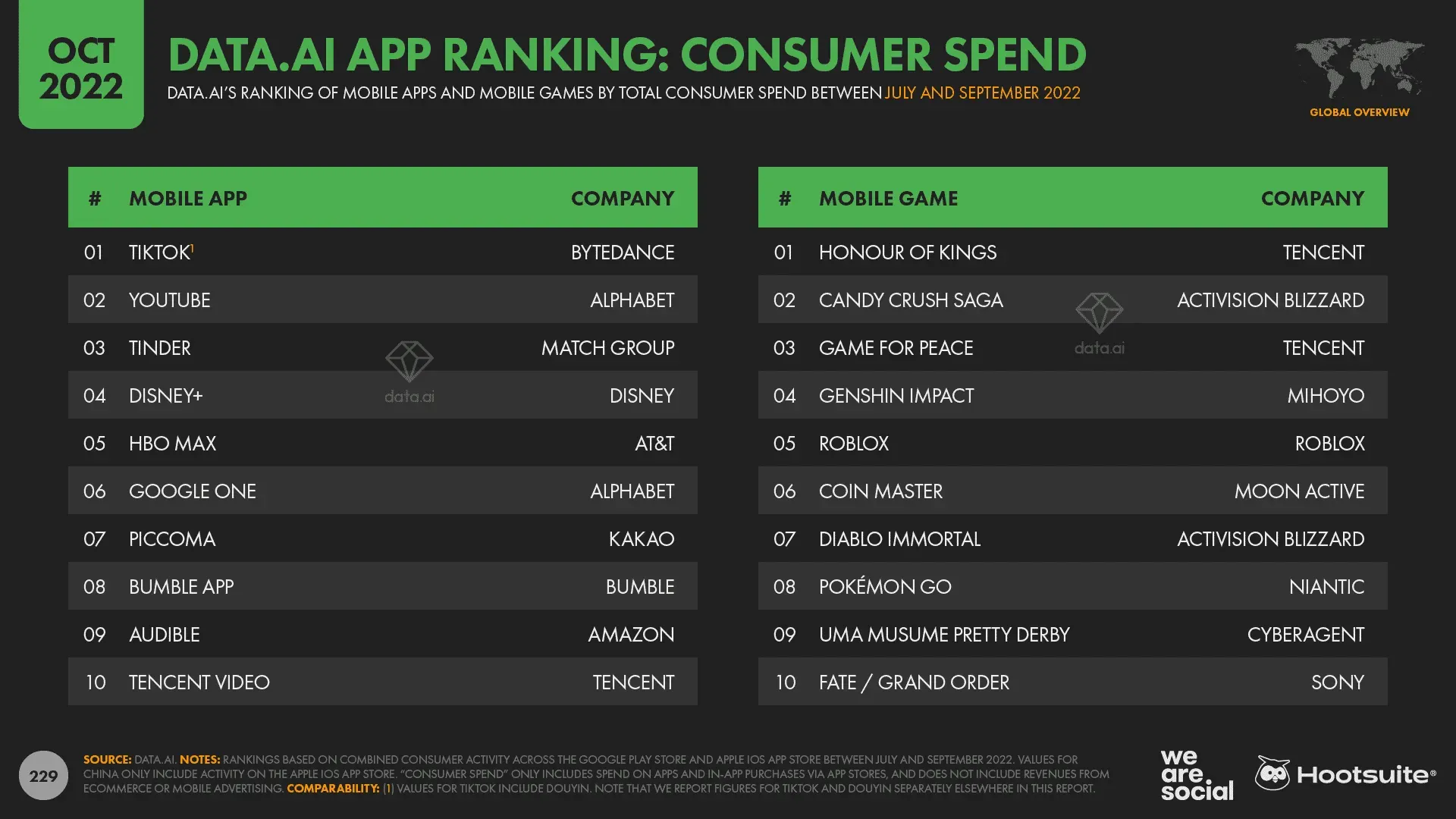

Sensor Tower analysis shows that TikTok’s global revenues, including spending on Douyin in China, reached over $914 million between July and September 2022, bringing its lifetime cumulative total to approximately $6.3 billion. United States (please note that we share user data for TikTok). and Douyin elsewhere in our reports.)

What’s more, this revenue figure only includes consumer spending on TikTok, which is primarily for the purchase of TikTok coins, and does not include the revenue that Bytedance generates from advertising.

Both data.ai and Sensor Tower report that TikTok was the top-grossing non-gaming mobile app in the world in the third quarter of 2022 based on combined consumer spending across the Google Play and Apple iOS stores.

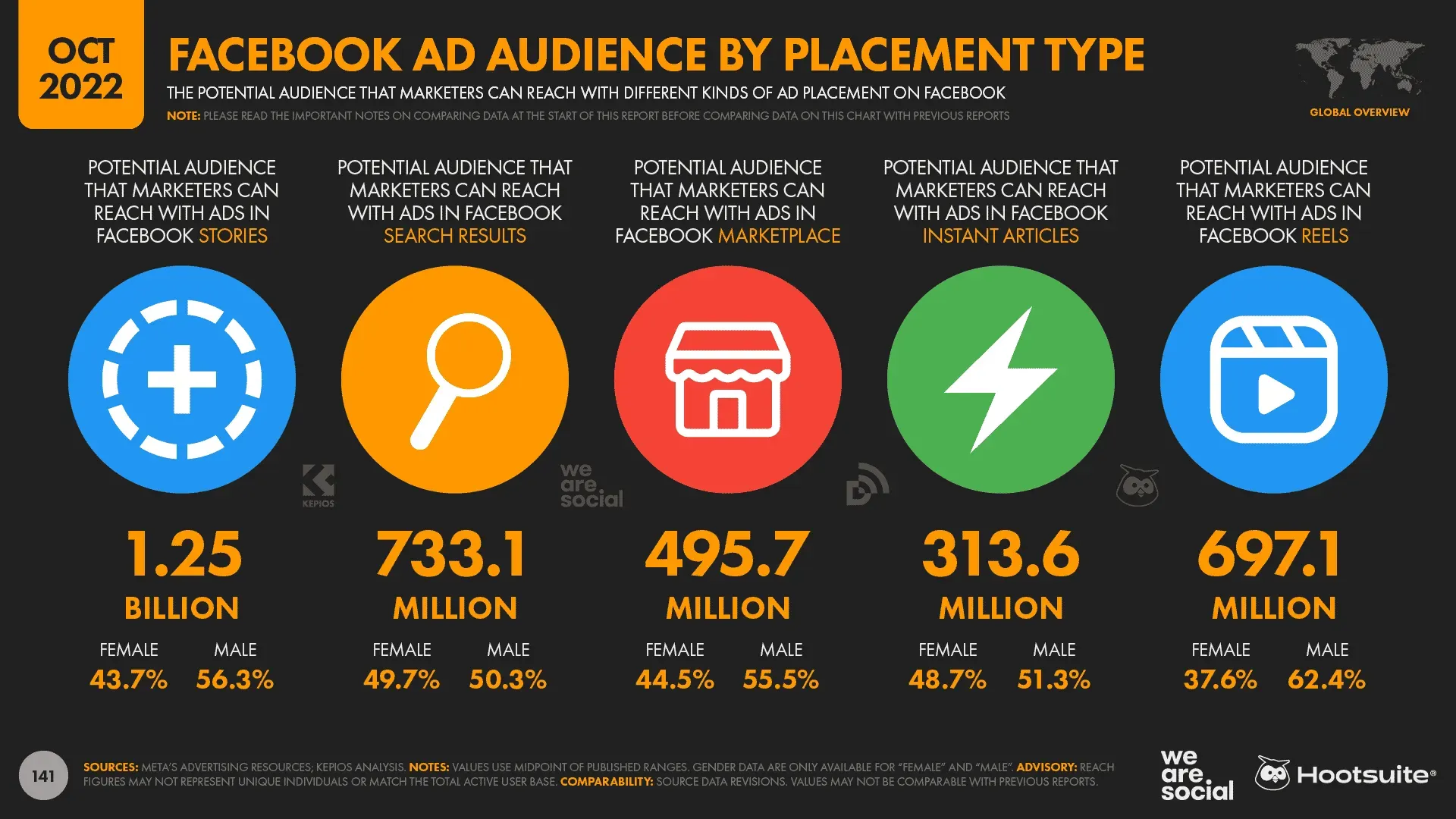

The reels keep spinning

The number of users that marketers can reach with ads in Meta’s Reels channels continues to grow.

Figures published in the company’s ad planning tools show that Facebook Reels’ global ad audience has jumped nearly 50% in the past three months.

The latest potential reach figure is just below 700 million users, reflecting an increase of over 220 million users since July 2022.

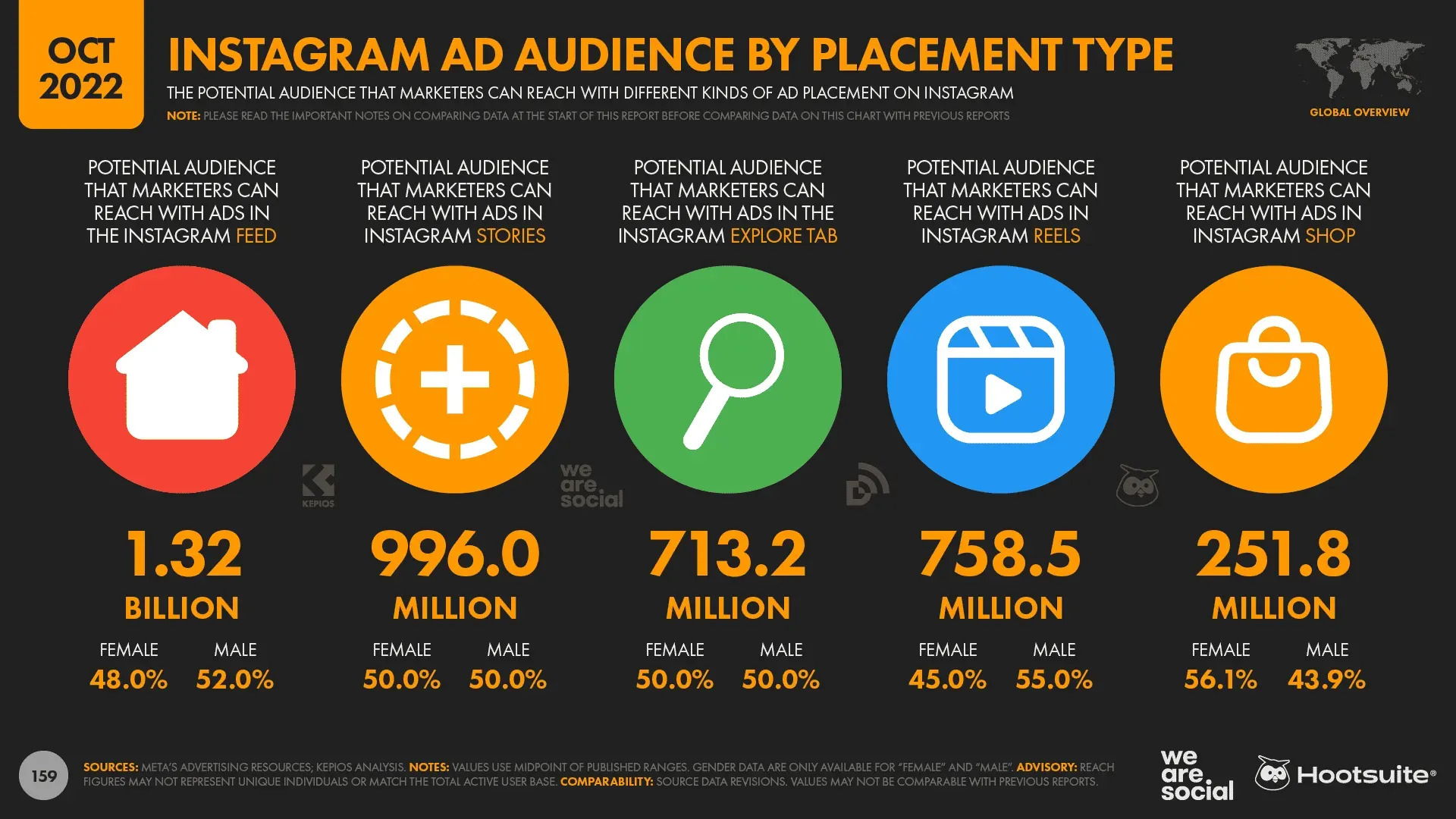

The number of users who see ads in the Reels Instagram feed has also increased since last quarter, albeit at a much more modest pace.

October 2022 data shows that Instagram Reels ads now reach 758.5 million users, up 0.5% from the 754.8 million users reported by Meta’s ad scheduling tools back in July.

Social networks are still popular on the Internet (not just in apps).

While it’s no secret that TikTok has added millions of users in recent months, the platform has seen another impressive growth that could come as a big surprise.

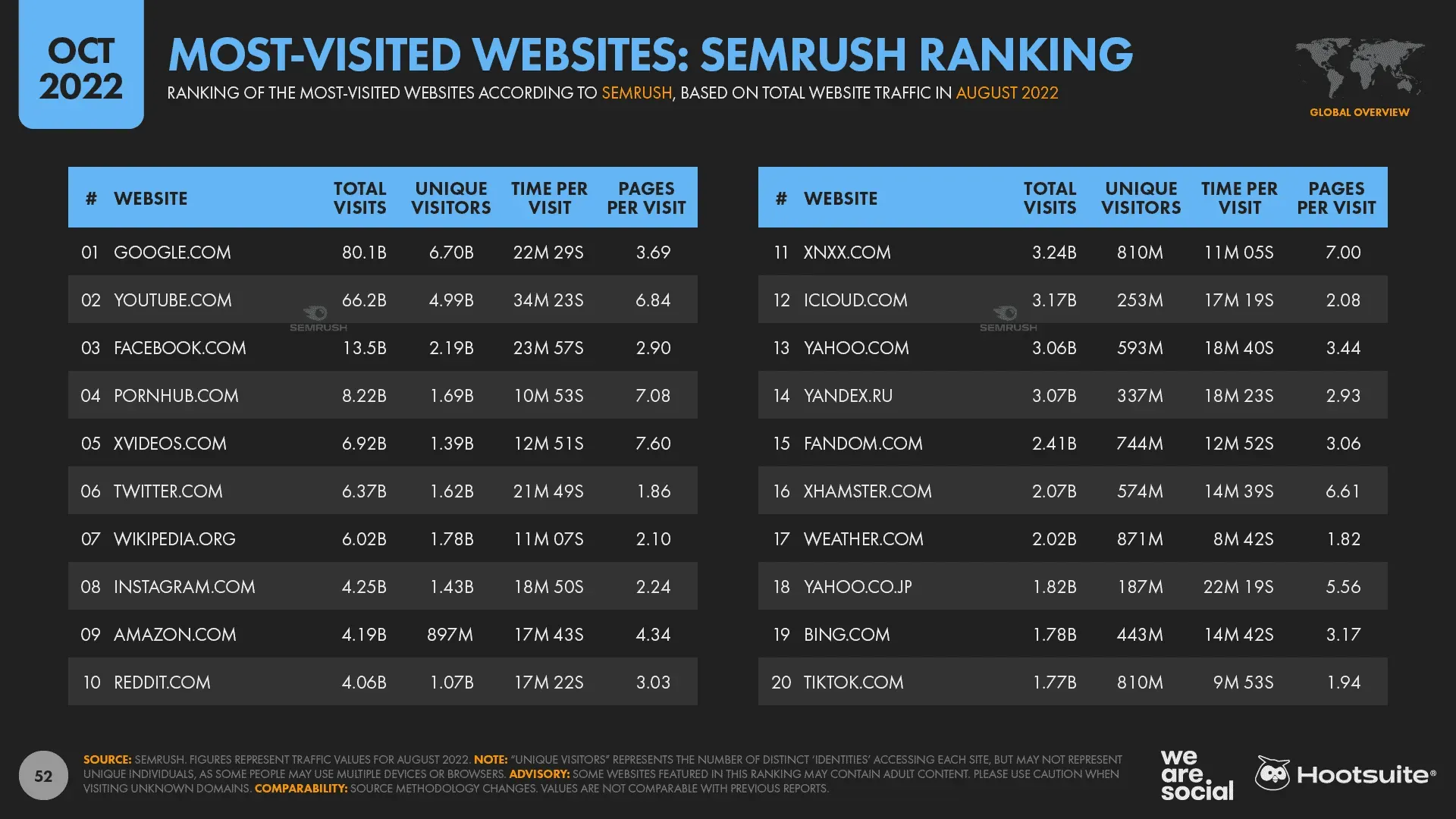

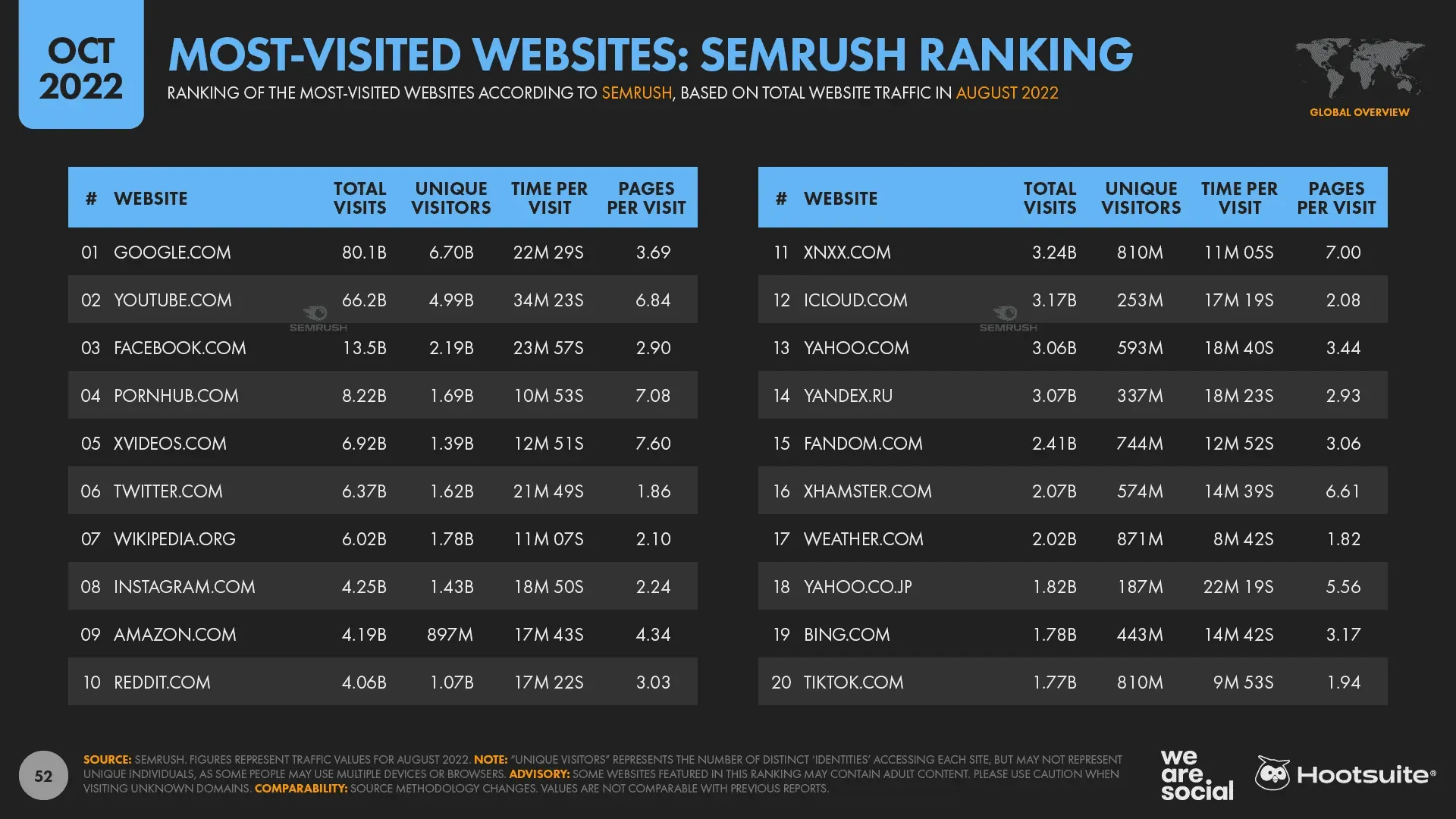

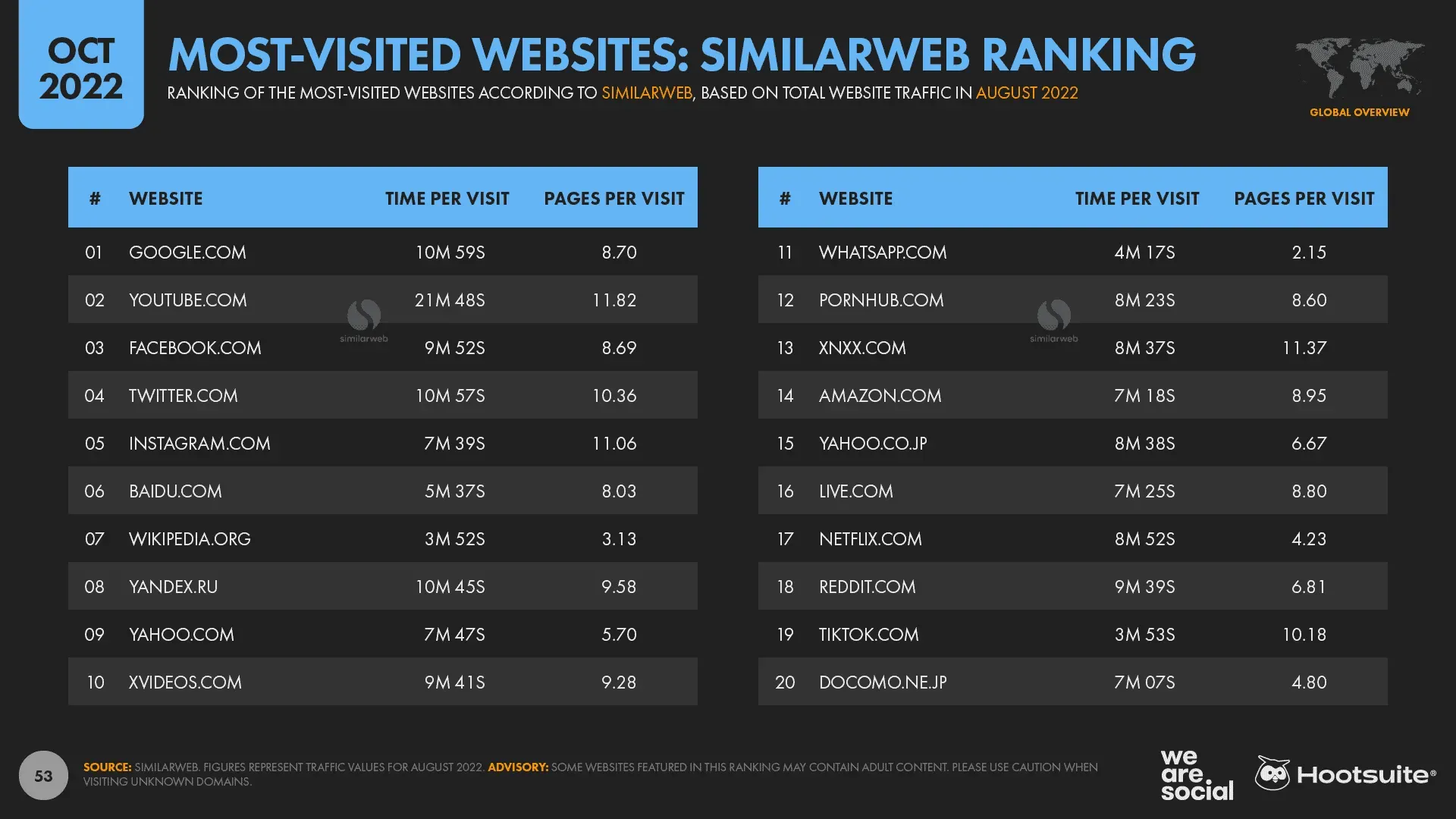

Both Semrush and Similarweb report that TikTok.com is in the top 20 most visited websites in the world.

In other words, TikTok is not just one of the largest mobile apps in the world; it is also one of the hottest properties on the internet.

To put this into perspective, Semrush reports that TikTok.com currently attracts over 800 million unique visitors per month, which could be more than half of the platform’s total active user base.

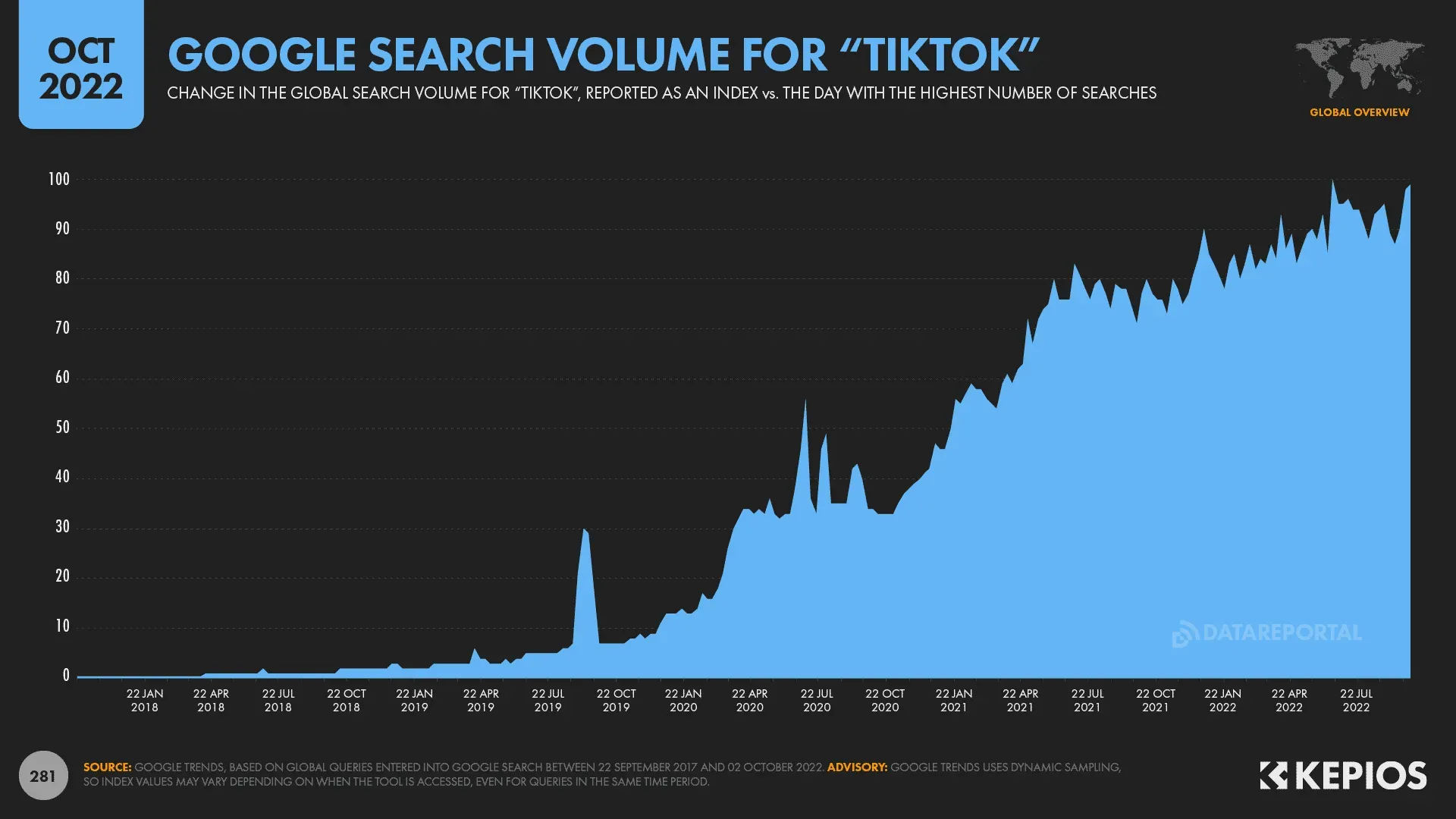

Meanwhile, Google Trends data also shows that “TikTok”searches have been steadily increasing in recent months.

For all queries typed into Google around the world between July 1 and September 20, 2022, TikTok ranked 25th in total search volume.

And given similar trends for Facebook, Instagram, and WhatsApp Web, there’s a good chance that many of these searches were done by people hoping to use TikTok content from a web browser rather than people who just want to know what TikTok is or download. application.

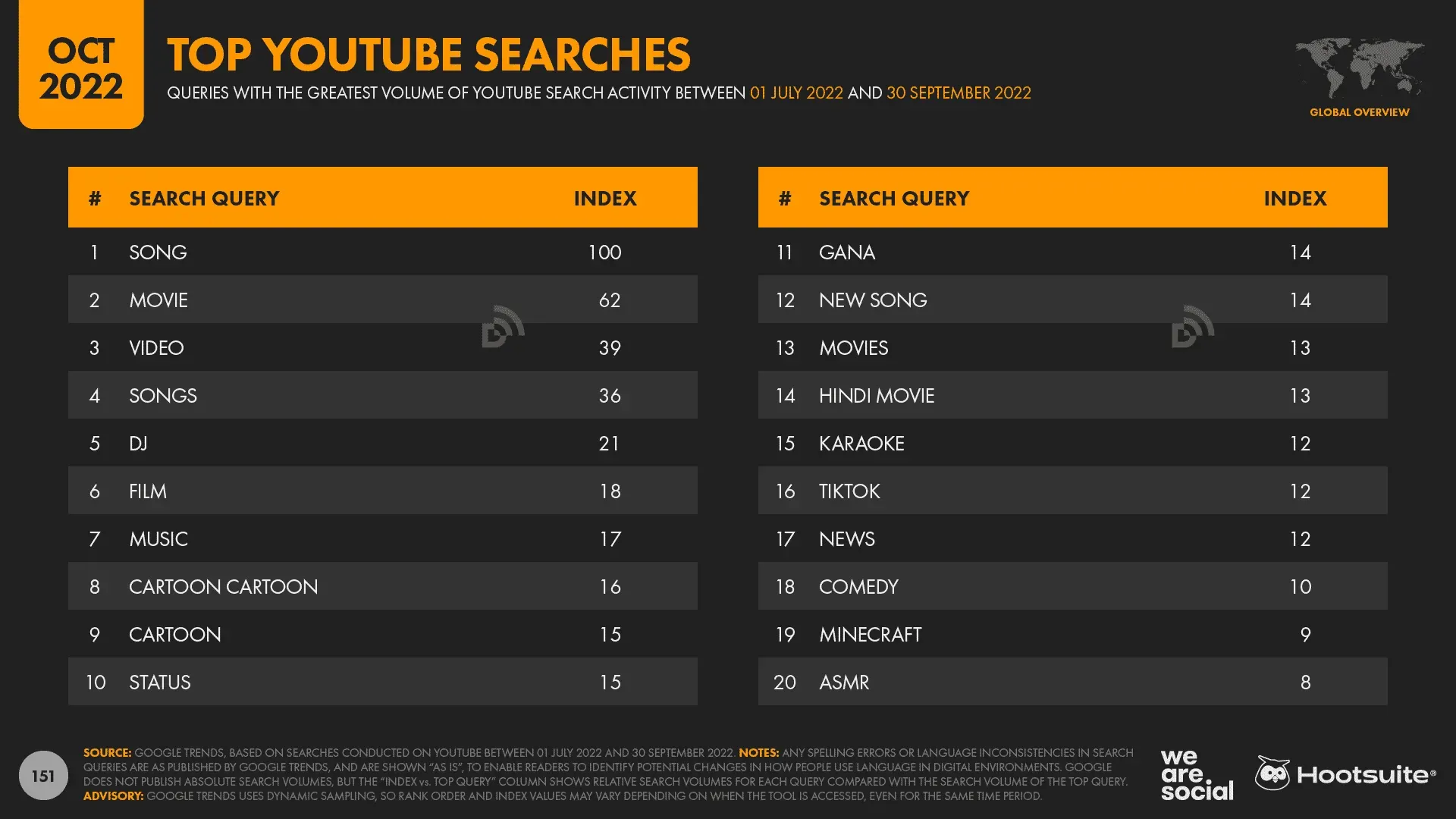

Also, it’s interesting to note that “TikTok”is currently the 16th most popular YouTube search in the world.

However, there is a certain irony in these search trends, given that Google executives are increasingly worried about the number of people who have shifted their search activity from search engines to social platforms.

There is little data to tell us whether TikTok’s web users are different from its mobile app users, but even if users should be the same, the usage context in a web browser is likely to be very different from that in the platform. application.

That being said, working with TikTok in a web browser is just as compelling, taking visitors directly to a “for you” feed without having to create or sign in to an account (try it out for yourself here).

It’s unclear if this rise in TikTok activity on web browsers has any special implications for marketers, but it’s worth considering if you’re planning TikTok content nonetheless.

But it’s important to note that this “social network”phenomenon is not unique to TikTok.

Semrush’s latest data shows that the websites of most of the leading social platforms continue to attract billions of unique visitors each month, though it’s worth noting that due to people’s use of multiple connected devices, these numbers can include a significant degree of duplication. when it comes to unique personalities.

YouTube sees the most unique visitors on its website, with Semrush reporting that a whopping 5 billion unique devices visited YouTube.com in August 2022.

Meanwhile, despite the company’s own data suggesting that app usage dominates access to Facebook, more than 2 billion unique devices also visited Facebook.com in August.

The Twitter and Instagram websites continue to attract over a billion unique visitors each month.

And the number for Twitter is particularly interesting because it suggests that a significant number of people continue to use the platform without logging in — and perhaps even without creating an account.

Similarly, despite the platform reporting a mere 50 million unique daily users, the Reddit website also attracts over 1 billion unique visitors every month, suggesting that many of the platform’s visitors do not register or log in.

And while it’s outside of Semrush’s current top 20, Similarweb reports that WhatsApp.com is also a favorite on the web, attracting more unique visitors than many of the world’s top adult sites.

Podcasts capture more people’s time

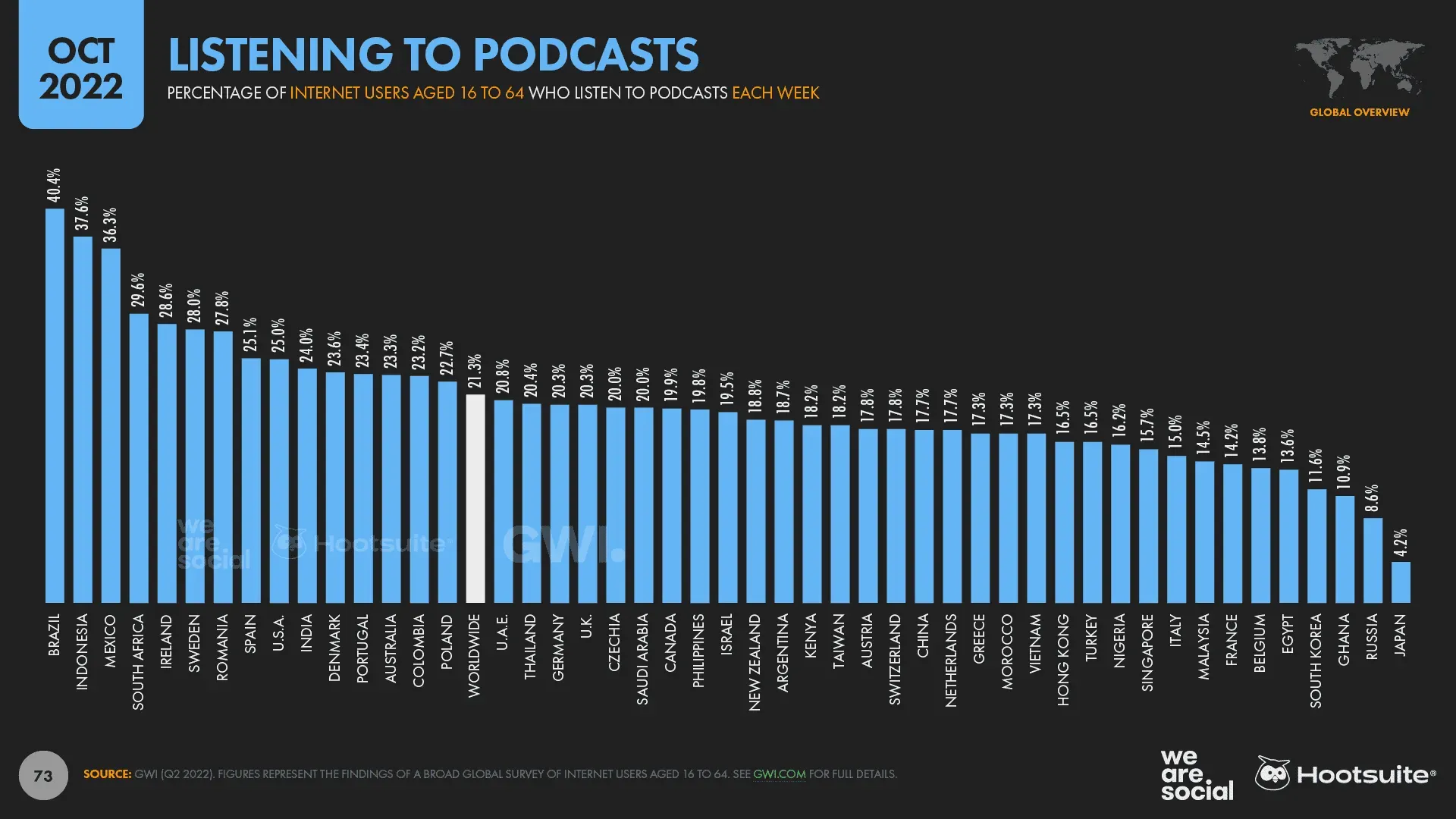

The latest GWI data shows that the typical working-age internet user now spends more than an hour a day listening to podcasts.

Globally, the average daily time spent listening to podcasts has increased by 7% over the past year, equating to an additional 4 minutes per day.

21.3% of Internet users aged 16 to 64 now listen to podcasts every week, averaging 61 minutes per day.

Looking ahead, these numbers show that working-age adults in the 48 countries covered by the GWI study will spend a total of more than 24 million years listening to podcasts in 2023.

It is interesting to note that the popularity of podcasts varies considerably across cultures, although there is no apparent pattern linking countries where podcasts are more or less popular.

Brazilians are the largest consumers of podcast content, with more than 4 out of 10 working-age internet users in the country saying they listen to at least one podcast every week.

On the other hand, the Japanese are the least likely to consume podcasts, with less than 1 in 20 working-age Internet users in the country saying they have listened to a podcast in the past seven days.

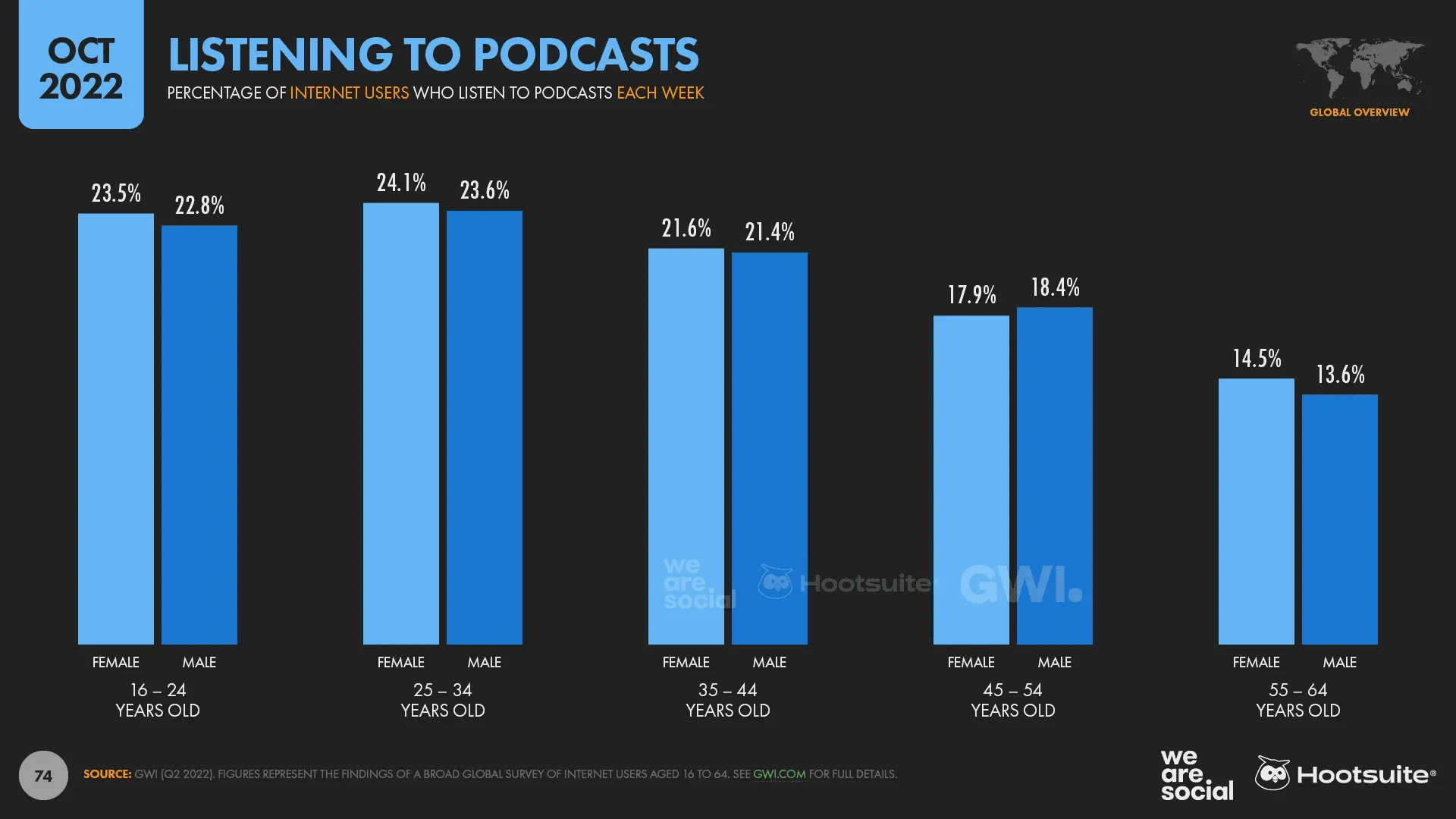

Younger age groups are more likely to listen to podcasts than their parents’ generation, although millennials are ahead of Gen Z when it comes to the proportion of internet users who tune in to podcasts every week.

It is also interesting to note that women are more likely to say they listen to podcasts than men, which may contradict the stereotype of the “typical” podcast listener.

Online shopping is better than email, music and more

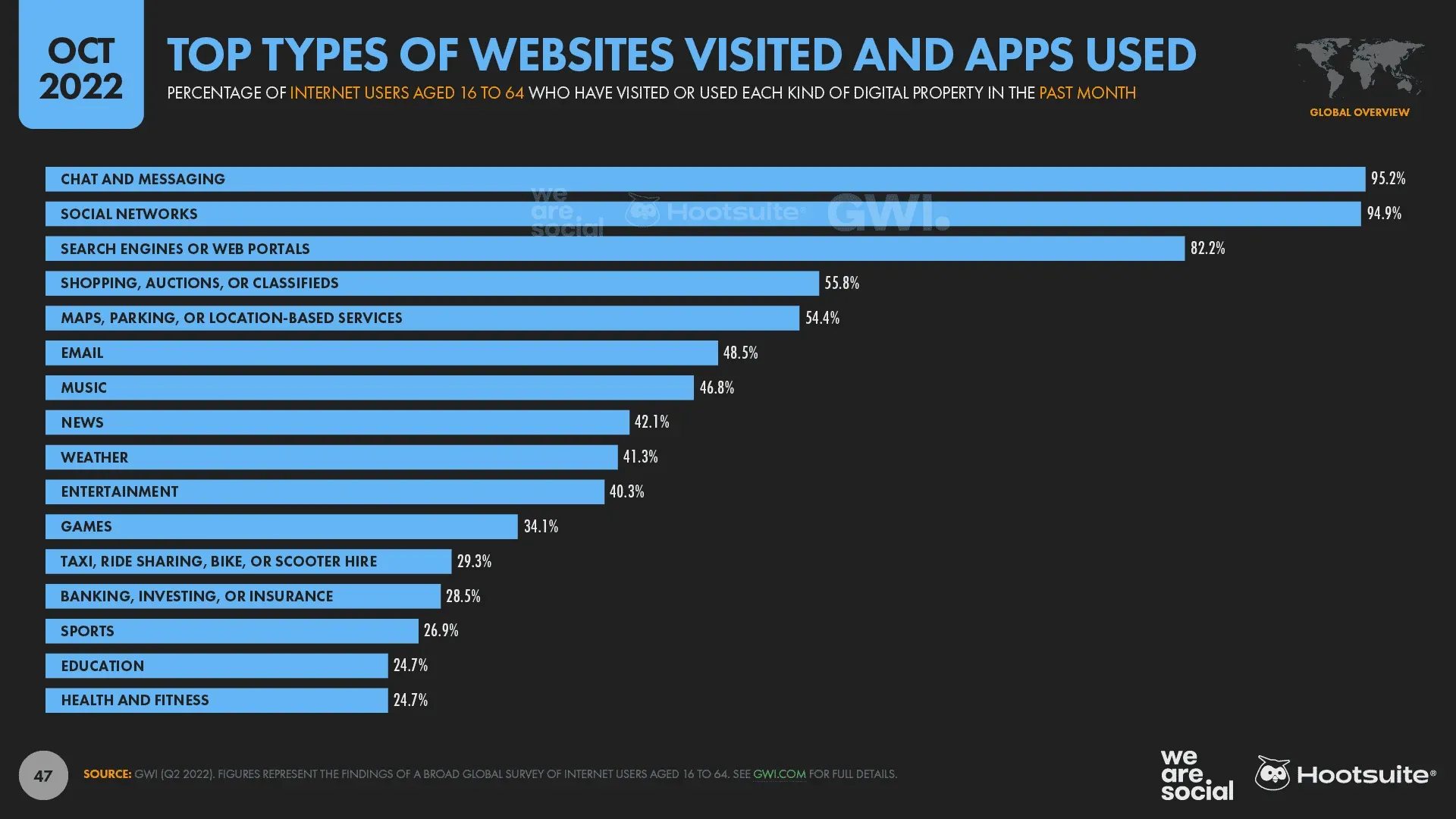

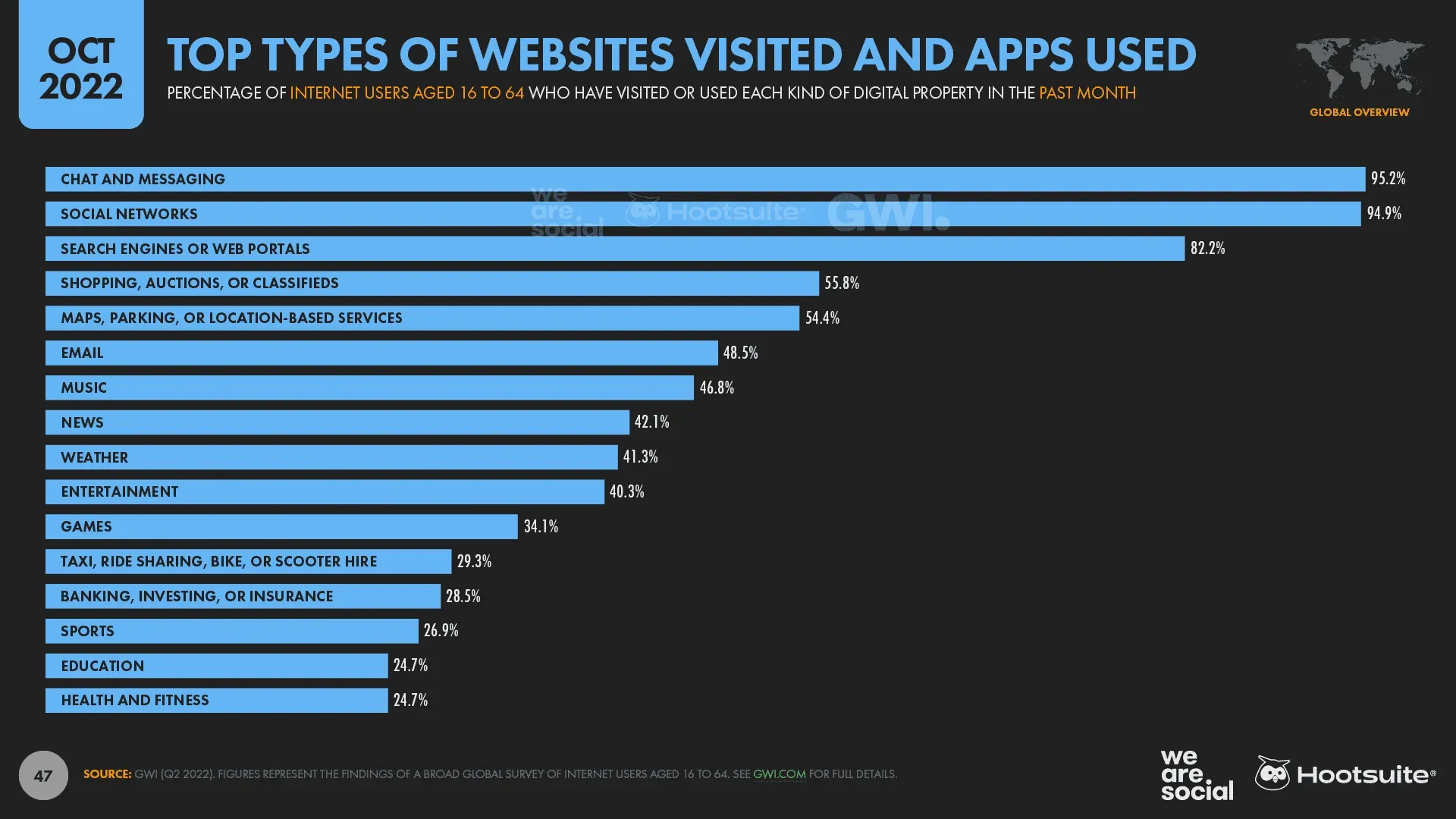

Shopping apps are ranked fourth in the latest GWI ranking of the types of websites and mobile apps people use each month.

Nearly 56% of the world’s working-age Internet users say they have used online shopping, auctions or classifieds platforms in the past 30 days, putting purchases ahead of email, music and even news and weather services.

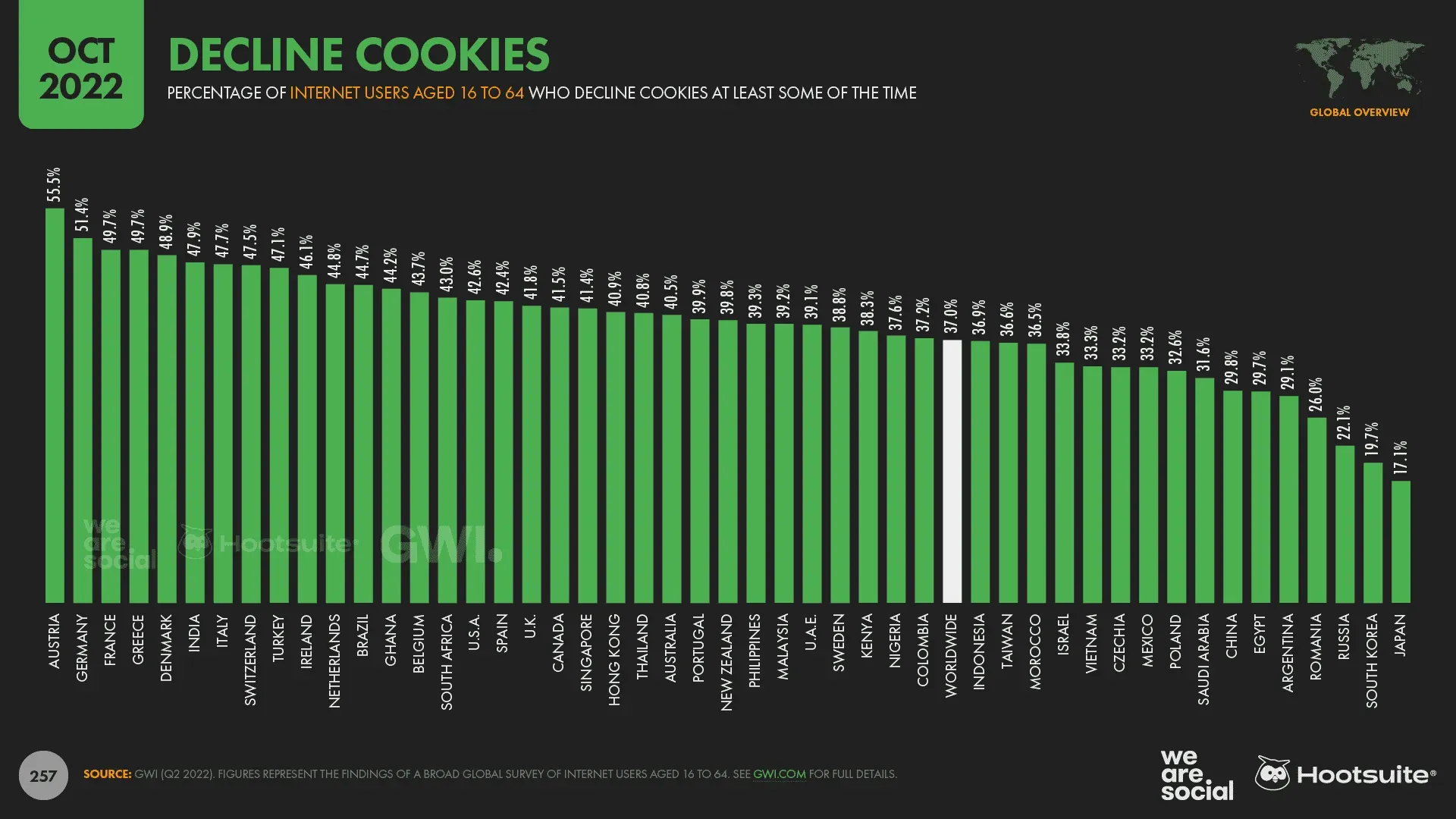

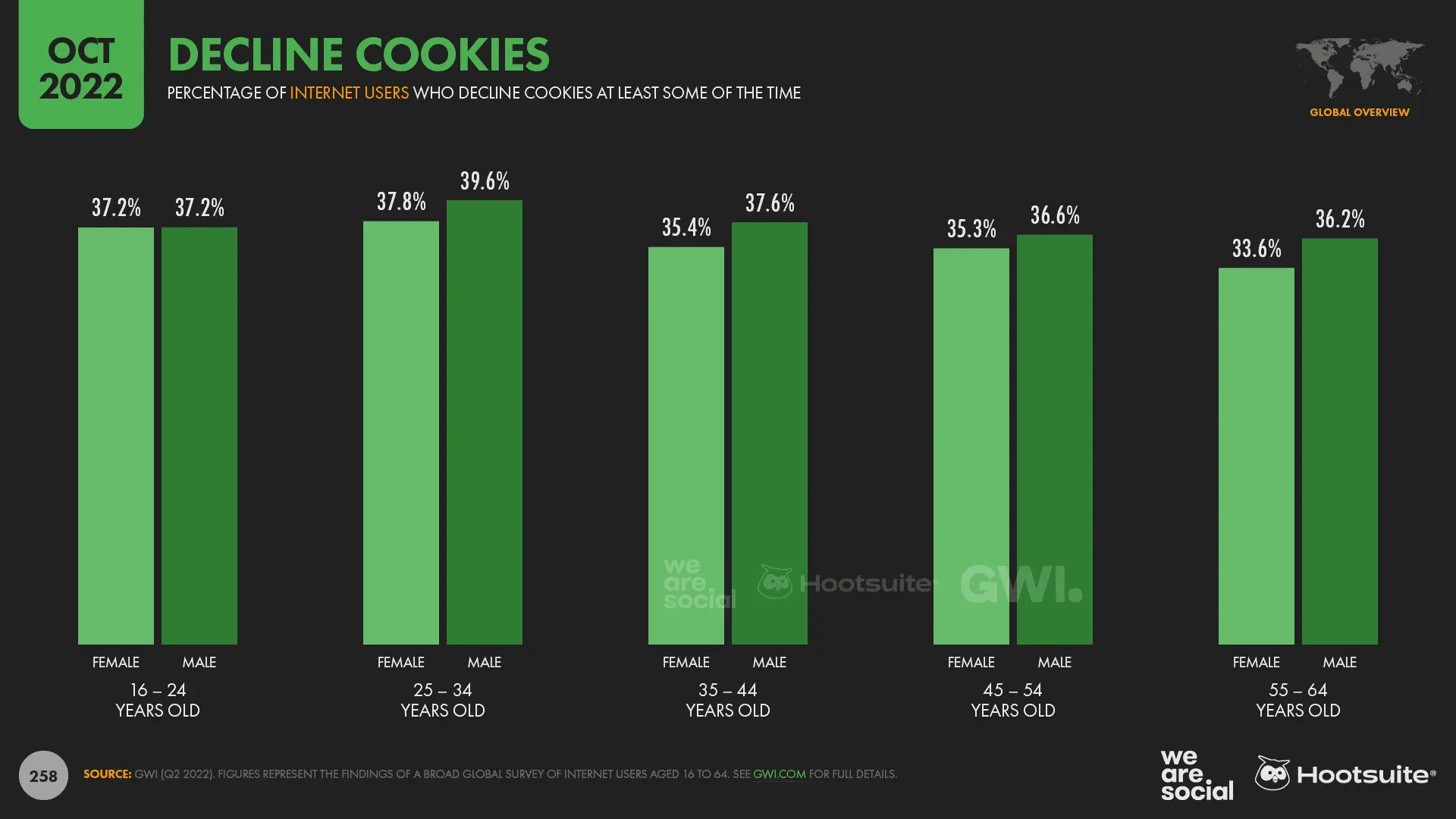

If you’ve ever read about online privacy, you might be surprised to learn that most internet users still accept cookies.

Globally, GWI found that barely 37% of working-age Internet users opt out of cookies at least occasionally.

Austrians and Germans are likely to opt out of cookies, with more than half of internet users aged 16 to 64 saying they are taking active steps to opt out of internet trackers.

On the other hand, less than 1 in 5 people in Japan and South Korea say they opt out of cookies at least once in a while.

Interestingly, however, attitudes towards cookies remain relatively similar across all age groups and genders, with younger users only marginally more likely to reject cookies than their parent’s generation.

Women are also somewhat less likely to refuse cookies, although differences between men and women are minimal.

So what do these numbers tell us?

Well, despite the collective hand-wringing from regulators in Europe and the ongoing industry debate about the legitimacy of cookies, it looks like most Internet users don’t really care.

Indeed, the data shows that even when given a choice, less than 4 in 10 of us are taking proactive steps to protect our privacy from these online trackers, suggesting that most people simply click “accept all”and move on.

This isn’t to say that digital platforms and marketers shouldn’t be doing more to protect people’s privacy, of course, but the evidence suggests that regulators and the media can do more with cookies than public opinion can justify.

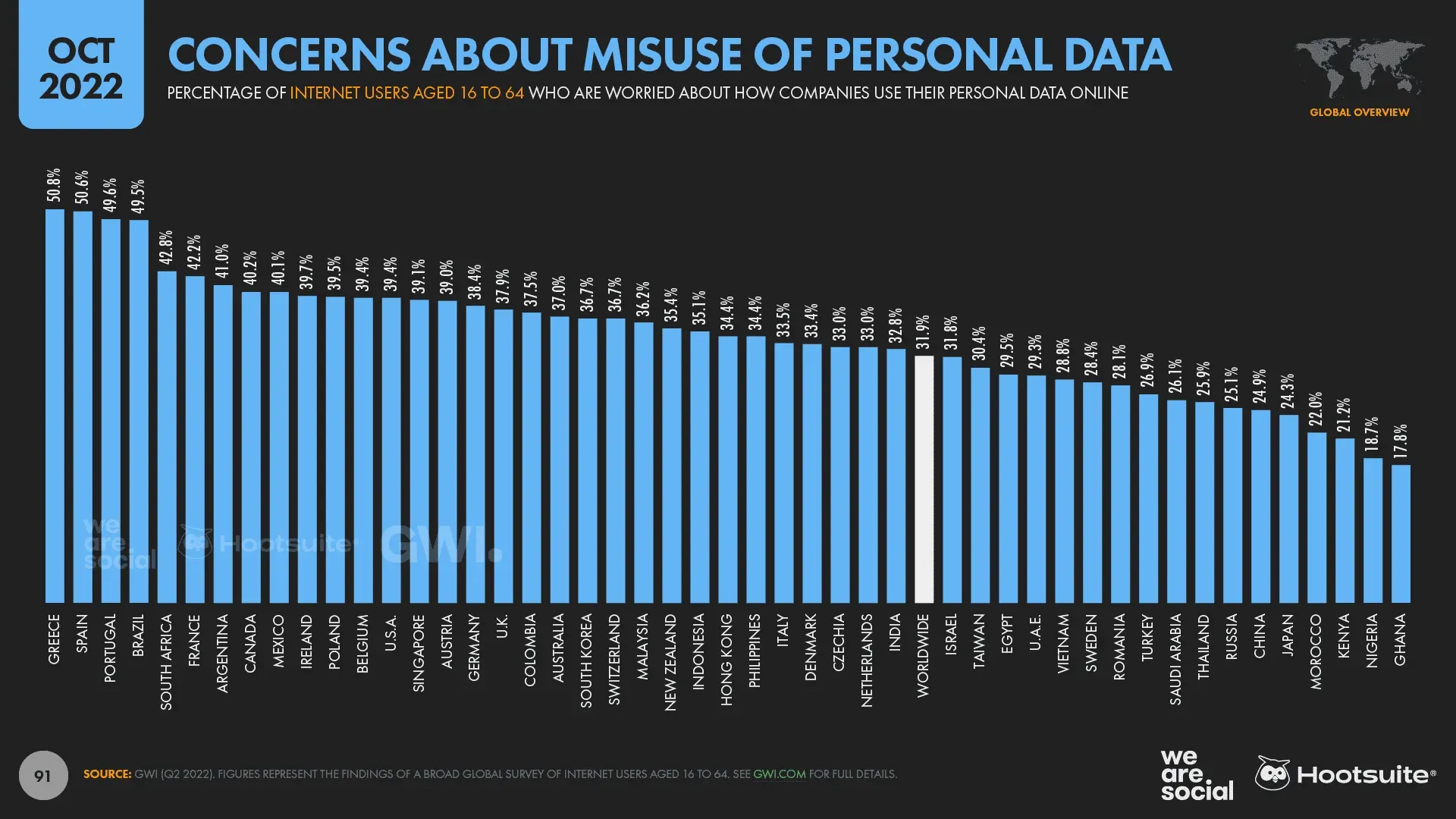

And there is more data in the GWI study to support this hypothesis: less than 1 in 3 internet users of working age say they are worried about how companies might use their personal data online.

Check out the latest data and insights on social media, the web, mobile and other digital technologies in the Digital 2022 report.

Important notes about changing data

Major Source “Fixes” to Social Media Ad Reach Metrics: Since our July 2022 report, Meta seems to have begun rethinking how it calculates and/or reports potential audience reach. Notes in the company’s ad scheduling tools suggest these changes are ongoing, but the numbers these tools now report for ad reach on Facebook, Instagram, and Messenger are already significantly lower than the numbers the same tools reported just a few months ago. We’ll look at these changes in more detail below, but please note that, as always, the latest data for these platforms may not be directly comparable to similar data published in our previous reports.

To learn more about other changes that may affect the comparability of data in the Global Digital Reports series, see our detailed data notes.